Is Your Human Capital Protected?

James Schofield - May 18, 2023

If you owned a money printing machine, would you buy insurance for it? You'd probably say yes. Now how about insurance to cover your earning potential, i.e. disability insurance? It's kind of the same thing.

Did you know that a 30-year-old making $70 K will earn more than $3.8 Million during his/her working years, assuming 2.5% increases every year? These earnings will go towards various life goals like down payments, childcare expenses, saving for retirement, and day-to-day expenses. Of course, achieving these goals will be impossible without earning an income, which is why your earning potential or human capital is by far your greatest asset, especially when you’re young. As financial planners, we sometimes ask the question, “if you owned a money printing machine, would you buy insurance for it?” For most reasonable people, the answer is yes, but when we ask if the same person owns disability insurance (DI), the answer is usually “no,” “I don’t know,” or “I think I have some through my work.” I believe the reason for the lack of awareness about the risk of disability is twofold; people can only visualize adverse scenarios in the context of something catastrophic, like an accident, but the reality is that most disabilities resulting in a 90-day or more absence from work are not because of an accident. The leading cause of disability claims is mental health-related issues such as depression and anxiety, accounting for 31% of claims[i]. We tend to be dismissive of mental health problems as issues that we won’t have to deal with, but just because they aren’t affecting us at the moment doesn’t mean they never will. For some reason, we tend to overestimate the amount of change that will occur in one year, but far underestimate the ways our lives will change over ten years.

According to reinsurance company Swiss Re, a $20 trillion-dollar gap exists in North America between the life insurance people need and what they have. If that number seems scary high, consider that there is much more general awareness about life insurance than for DI. Based on the amount of liability, there is a far greater need for DI because the risk affects every person who earns an income, not just people with dependents. Considering the lack of awareness and even greater need, I’m guessing the need gap would be even higher for DI. There are only two questions people should ask themselves to determine if they need DI. Do I depend on my income, and do I have disability insurance? If the answer to the first question is yes and the second is no, you should secure DI coverage as soon as possible. If the answer to the second question is yes, you may need additional DI coverage depending on the structure of your work-sponsored plan. If you’re thinking of filing this task in the not urgent quadrant of your Eisenhower matrix, consider this: the chance of a 30-year-old male suffering a disability lasting longer than 90-days is 20% and 25% for females, much higher than the mortality rate for a 30-year-old. When a disability lasts longer than 90 days, the average length is between 2.1 and 3.2 years[ii]. Long enough to completely alter your future.

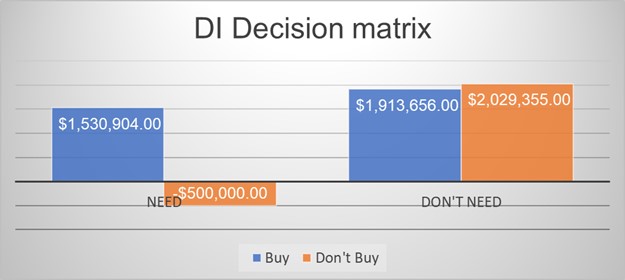

Your financial plan should help clarify any significant financial decision and like a snowflake; no two plans are exactly alike. The example below illustrates the one decision-two outcomes matrix you should use to evaluate the decision about purchasing disability insurance[iii]:

[i] World Health Organization — Disease and injury country estimates (November 2013) 4

[ii] 4 1985 Commissioners Individual Disability Table A

[iii]The bar chart graph above makes the following assumptions:

- - spouse 1 earns $120,000.

- - spouse 2 earns $55,000.

- - Couple’s ages are 49 & 47 in 2019.

- - Planned retirement at age 62 and 60.

- - currently spending $94,000 per year.

- - Saving 12% of gross earnings.

- - Mortgage of $150,000 outstanding.

- - Spending in retirement reduced by 15%.

- - disability premiums for the higher-earning spouse are $270/month.

- - disability benefit is $6,000 tax free/month.

- - Disability occurs in 2024 and lasts for the remaining working years.

- - In the don’t need scenario, $270/month is saved instead of buying DI.

- - In ‘the need, don’t buy’ scenario, the couple sells the house, and the runs out of money at age 78/76.

- - In the three successful scenarios, the home is not sold, and life expectancy is 95 for both spouses.

- - investments earn a 5% rate of return after fees.

- - minimum retirement age for a successful plan is 59 for the high earner.