A Smooth Start (For Now)

Alfred Lam - Feb 24, 2023

January produced impressive gains at asset class level as last year’s headwinds became this year’s tailwinds. But with many risk factors still looming, will it last?

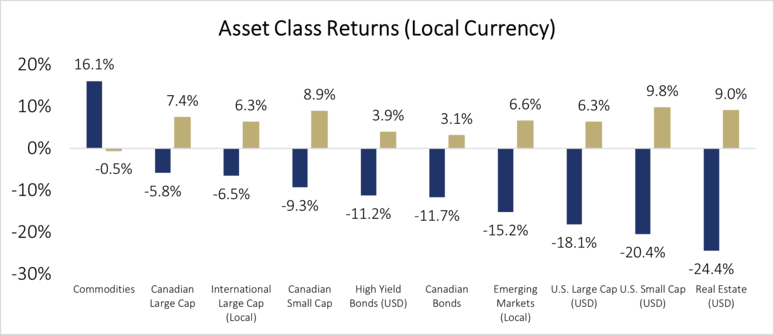

Investors’ appetites have increased as we entered 2023. Generally, at asset class level, the larger the loss in 2022, the larger the gain (recovery) in 2023, though this is only the data for January (see chart below).

What made investors so optimistic?

We recognize investors are feeling reassured by progress on several issues: First, China exited their restrictive zero-COVID policy and is now fully reopened. Second, inflation is cooling and there is confidence it will gradually decline to 3% in 2023. As a result, central banks will at least pause hiking rates in the coming months. Third, the Russia/Ukraine situation, while unresolved, is also not getting worse. Last but not least, Europe was able to maintain healthy natural gas inventory as the winter was warmer than usual, hence lower drawdown.

Source: Morningstar Research Inc., Bloomberg Finance LP, as of January 31, 2023. Asset class returns are based on the following: Commodities: Bloomberg Commodities Index TR USD; U.S. Large Cap: S&P 500 TR USD, High Yield: ICE BofAML U.S. High Yield TR USD, U.S. Small Cap: Russell 2000 TR USD, Canadian Bonds: FTSE Canada Universe Bond, U.S. Bonds: Bloomberg US Aggregate Bond TR USD, Real Estate: FTSE EPRA NAREIT Developed TR USD, Intl Large Cap: MSCI EAFE GR LCL, Canadian Large Cap: S&P/TSX Composite TR, EM Equity: MSCI EM GR LCL, Canadian Small Cap: S&P/TSX Small Cap TR, Global Large Cap: MSCI World GR LCL.

The impact on portfolios

The gains have been impressive considering the very short time frame. Our portfolios have had a similar experience: “recovery ratio” and performance were enhanced due to stronger performance in equity driven by an overweight allocation to China, small caps, and real estate. Hedging a portion of our USD exposure also added value. On the other hand, an overweight energy position was a detracting factor in January.

Will it last?

We do not expect the next 11 months to be as smooth as January. Some of the good news has been baked into asset prices, as we’ve seen from recent market rallies. We have made some adjustments including raising cash (which now has a yield of 4%), trimming bonds, and reducing Chinese and U.S. equity exposure. Cash will be re-deployed when opportunities arise but must at least beat the 4% return hurdle. This means we will probably return to purchasing equity before bonds, bearing in mind a 10-year Canadian bond only yields 3.1% today (Feb 9, 2023).

Overall, January produced impressive asset class returns as 2022’s drawdowns quickly became 2023’s gains, at least for the time being. Investors were reassured by cooling inflation, China’s reopening, Europe evading a fuel crisis, and a lack of escalation in the Russia-Ukraine war. Portfolios benefitted from allocations to China, small caps, real estate, and hedging USD exposure.

About the Author

Alfred Lam

Alfred Lam, Senior Vice President, Co-Head of Multi-Asset, joined CI GAM in 2004. He brings over 23 years of industry experience to his portfolio design, asset allocation, portfolio construction, and risk management responsibilities, which include chairing the multi-asset investment management committee and sizing investment bets to drive added value and manage risk. Alfred holds the CFA designation and an MBA from York University Schulich School of Business. He is a recognized leader in multi-asset investing in Canada. During his tenure, his team has won multiple investment awards, including the Morningstar Best Fund of Funds, and saw assets growing four-fold.