Market Pulse - The week in review

Duncan Presant - Feb 01, 2023

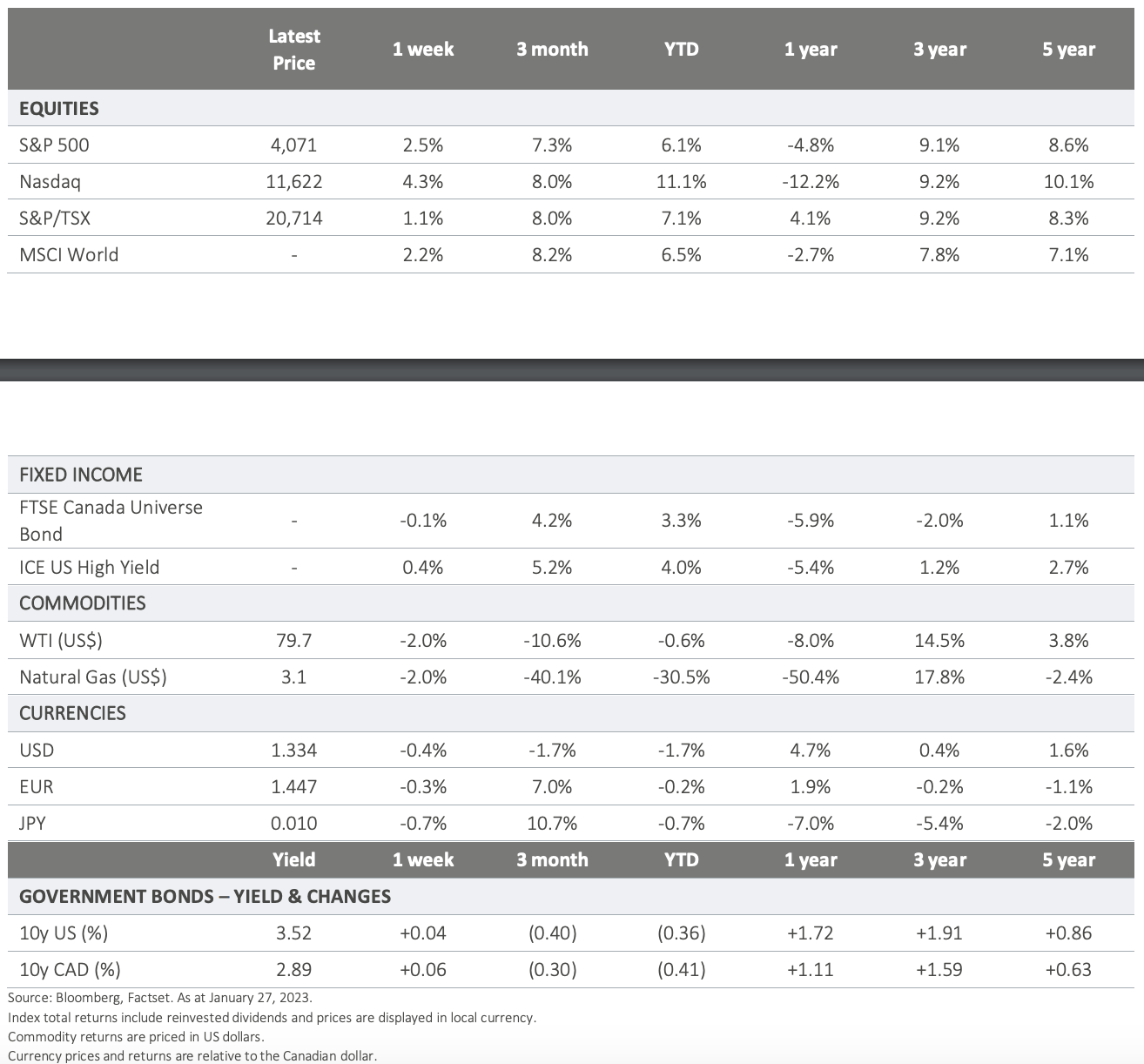

THIS WEEK’S RECAP: ▪

The Bank of Canada increased its target rate by 25 basis points (bps) to 4.5%. Consistent with our expectations, Governor Macklem indicated that monetary policy is now on hold as they pause to monitor the impact of previous rate hikes. They lowered their inflation projections to 3.6% for this year and 2.3% for 2024. The bank also lowered its forecast for economic growth by half for 2023 (from 1% to 0.5%), in part due to weaker foreign demand and a further slowdown in the housing market.

▪ In Europe, the outlook continues to improve as evidenced by optimistic consumer sentiment and business expectations survey results this past week. The positive shift was also reflected in local Purchasing Manager Indices (PMIs) which have seen a strong recovery from the lows, both in manufacturing and services. A very mild start to the winter has significantly reduced the risk that energy supplies would be insufficient, which was one of the main tail risks for the European economy.

▪ The bond market is increasingly anticipating a reversal of Fed policy (rate cuts) into the latter part of this year as inflation pressures ease and the strength of the labour market implies strong household and corporate balance-sheets that can withstand heightened interest rates for a short period of time. The prospect of lower rates and a relatively resilient economy have supported equity markets so far this year.

▪ While this goldilocks combination of lower inflation and resilient economy is probably helped by the recent change in narrative from central bankers, we believe that it is important to keep in mind that uncertainty remains high. Consumer prices fell in December, and annual inflation in the U.S. may drop below 2% this year due to lower energy and goods prices, which is obviously a very welcome development. However, as inflation drops, GDP growth is also decreasing, retail sales and industrial production have fallen in December, and indicators of output are sharply down while inventories mount, which often indicates a potential recession. The labour market is currently the strongest aspect of the economy, but it usually tends to lag the economic cycle. Continued strength could make it harder for central bankers to soften their stance on the monetary policy front. We remain cautiously optimistic but continue to closely monitor the situation.

ON DECK FOR NEXT WEEK:

▪ The Federal Open Market Committee (FOMC) is widely expected to raise their target rate by 25 bps on Wednesday. While there have been some calls for a 50 bps increase, we believe this would be at odds with recent inflation dynamics and, more importantly, with the change of tone that several of the Fed officials have adopted in recent public interventions.

▪ On Thursday, the Bank of England is expected to raise rates by 25 or 50 bps. The European Central Bank will also meet Thursday and is expected to deliver a well telegraphed 50 bps hike (with more to follow as they play catchup relative to other major central banks in the fight on inflation).

For more information, please visit ci.com.

IMPORTANT DISCLAIMERS: This document is provided as a general source of information and should not be considered personal, legal, accounting, tax or investment advice, or construed as an endorsement or recommendation of any entity or security discussed. Every effort has been made to ensure that the material contained in this document is accurate at the time of publication. Market conditions may change which may impact the information contained in this document. All charts and illustrations in this document are for illustrative purposes only. They are not intended to predict or project investment results. Individuals should seek the advice of professionals, as appropriate, regarding any particular investment. Investors should consult their professional advisors prior to implementing any changes to their investment strategies. Certain statements contained in this communication are based in whole or in part on information provided by third parties and CI Global Asset Management has taken reasonable steps to ensure their accuracy. Market conditions may change which may impact the information contained in this document. CI Global Asset Management is a registered business name of CI Investments Inc. © CI Investments Inc. 2023. All rights reserved.