Market Pulse - The week in review - June 19th

Duncan Presant - Jun 21, 2023

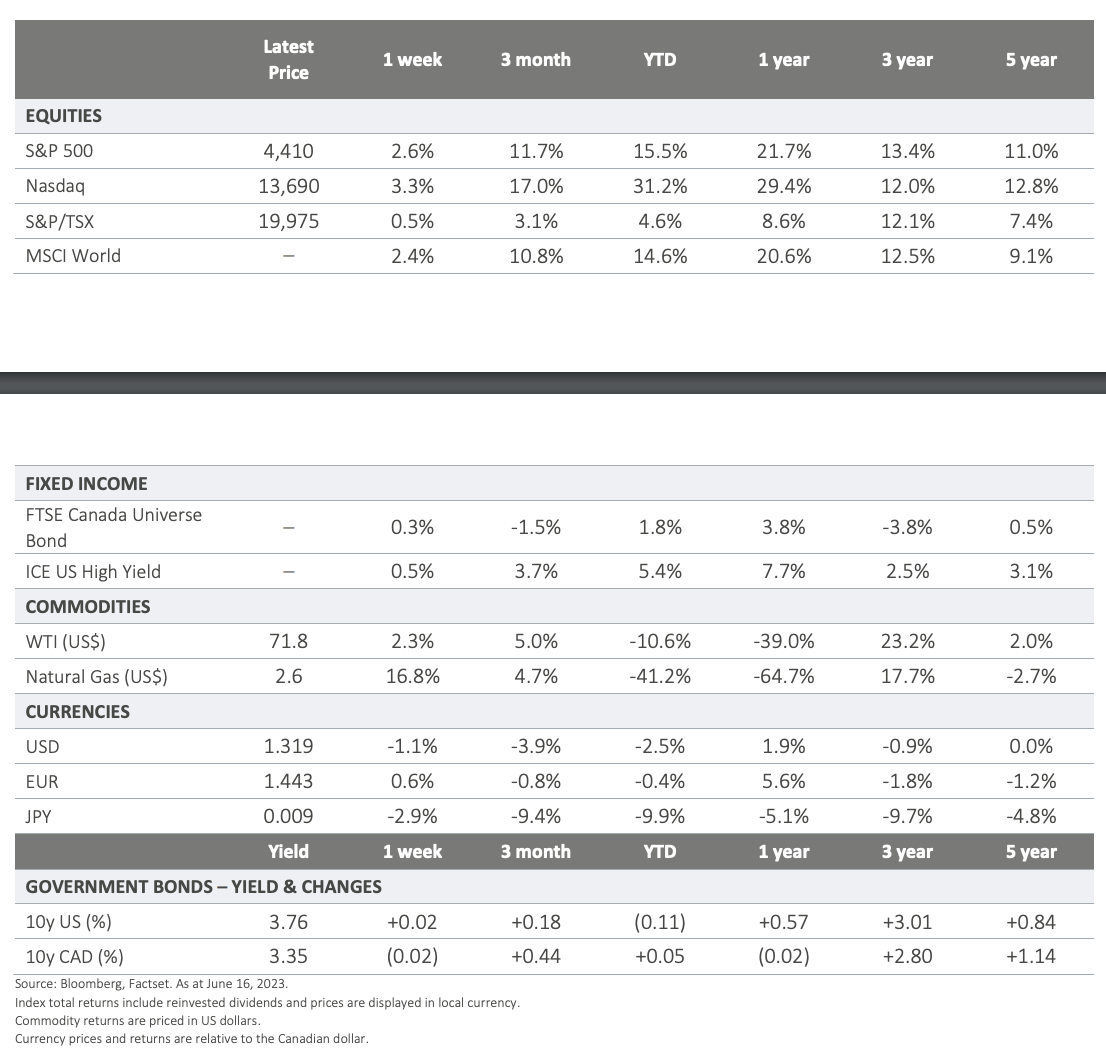

US inflation remains elevated, particularly when stripping out energy and food prices. Core CPI was up 0.44% in May, supported in part by higher shelter and used car prices.

THIS WEEK’S RECAP:

▪ US inflation remains elevated, particularly when stripping out energy and food prices. Core CPI was up 0.44% in May, supported in part by higher shelter and used car prices. On the positive front, Jerome Powell’s preferred super-core measure (core services excluding rent of shelter) increased at a far more comfortable pace of 0.2%. The good news is that inflation pressures are easing, albeit at a very slow pace which will require high interest rates for a considerable period.

▪ The Federal Reserve took a hawkish pause, leaving their target rate unchanged as widely expected. The heavy lifting on rate hikes is now behind us, going forward it will be a matter of making smaller, incremental adjustments to policy if necessary. The Fed will allow for the aggressive policy tightening (+5% over the past year) to take hold, particularly given the uncertainty surrounding long and variable lags to inflation and the economy. Broader demand (consumption) takes longer to adjust to higher rates, which is in part why it makes sense to slow the pace of rate hikes at this juncture.

▪ The monthly survey of US small and medium size businesses gauges (NFIB) provided some reassuring data points that the downturn in hiring, sales expectations and credit availability have at a minimum slowed. However, the outlook amongst respondents remains quite bleak, an ominous signal that continues to flash red despite an economy that refuses to die in the face of weak leading economic indicators.

▪ The European Central Bank (ECB) raised their target benchmark rate to 3.5%. The BCE also raised its 2023 forecast for core inflation to 5.1% (up from 4.6% in March), reinforcing the likelihood of further rate hikes. President Lagarde was prescriptively hawkish in her comments, though reiterated the future policy path continues to be highly data dependant.

▪ Fragile geopolitical relationships show signs of improvement as Iran and the US explore a potential agreement to ease sanctions in exchange for assurances on nuclear weapon development. Additionally, US Secretary of State Blinken's upcoming visit to Beijing, following its previous cancellation, indicates efforts to repair strained diplomatic ties with China.

ON DECK FOR NEXT WEEK:

▪ The last of the major central bank announcements comes from the Bank of England, they are expected raise rates by 25bp to 4.75% Thursday morning. Otherwise, economic releases will be mostly second tier type data are not expected to be major market drivers.

▪ With US and global equities surpassing the highs of last summer, market watchers are closely monitoring the extent to which the narrow technology sector rally will extend its influence across other sectors. However, there is a growing sense of caution as the participation levels (volumes) have remained conspicuously light, prompting concerns about the sustainability of this upward momentum in the market.

For more information, please visit ci.com.

IMPORTANT DISCLAIMERS

This document is provided as a general source of information and should not be considered personal, legal, accounting, tax or investment advice, or construed as an endorsement or recommendation of any entity or security discussed. Every effort has been made to ensure that the material contained in this document is accurate at the time of publication. Market conditions may change which may impact the information contained in this document. All charts and illustrations in this document are for illustrative purposes only. They are not intended to predict or project investment results. Individuals should seek the advice of professionals, as appropriate, regarding any particular investment. Investors should consult their professional advisors prior to implementing any changes to their investment strategies. Certain statements contained in this communication are based in whole or in part on information provided by third parties and CI Global Asset Management has taken reasonable steps to ensure their accuracy. Market conditions may change which may impact the information contained in this document. CI Global Asset Management is a registered business name of CI Investments Inc. © CI Investments Inc. 2023. All rights reserved.