Market Pulse - The week in review - Aug. 18th 2023

Duncan Presant - Aug 28, 2023

Worries are rising around China’s economy and the potential impact it has on its official and shadow banking systems are mounting.

THIS WEEK’S RECAP:

▪ Worries are rising around China’s economy and the potential impact it has on its official and shadow banking systems are mounting. China’s delayed reopening relative to the rest of the world had created hopes that its economic rebound would support global growth in 2023. While it is now clear that the rebound is not as strong as expected, it is difficult for global investors to get a full grasp of the situation, which leads to speculation and mounting fears. This week saw a series of support measures announced by Chinese authorities, which in a certain sense reinforced the view that the situation is serious. We are closely monitoring the situation but think that fears might be overblown.

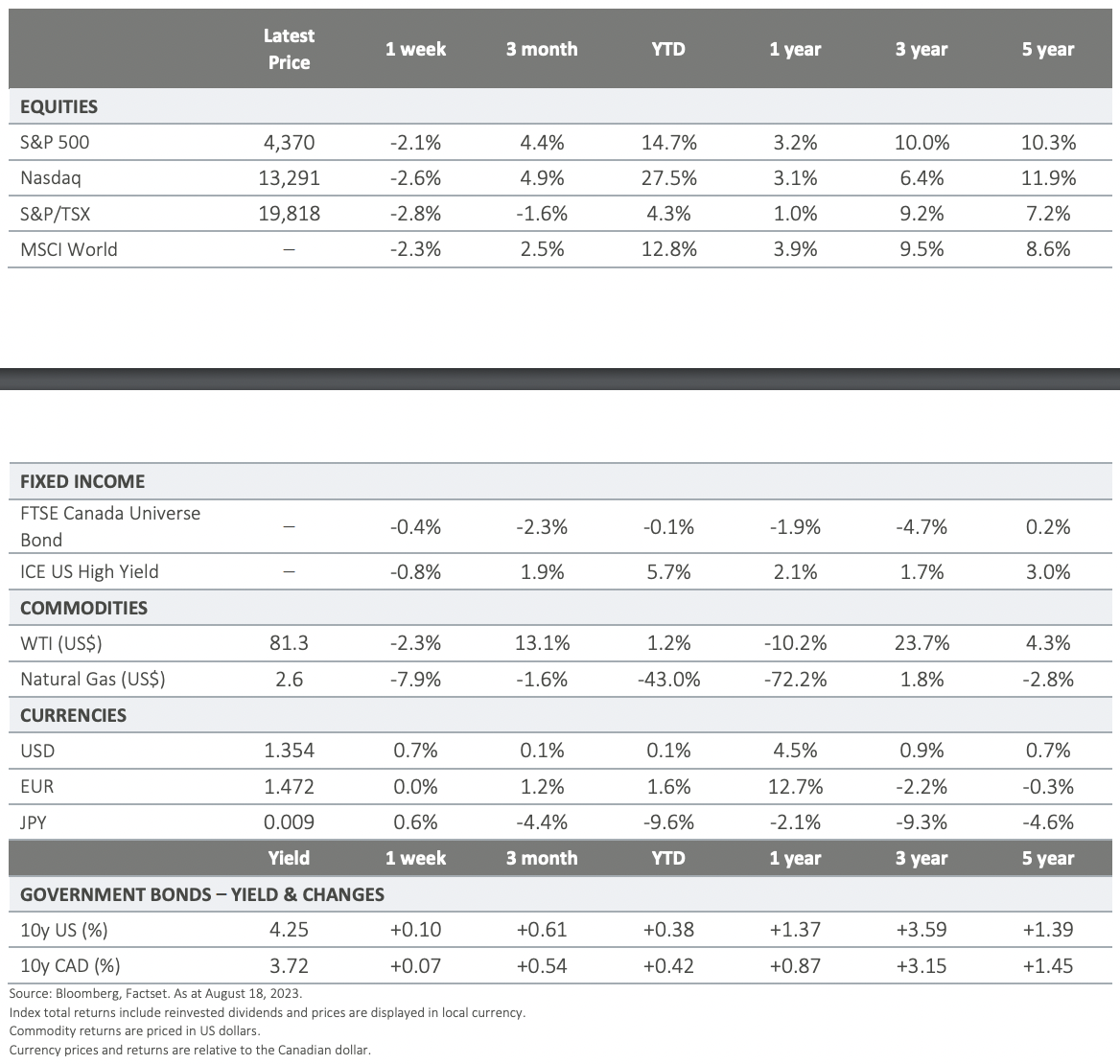

▪ Canada’s July inflation numbers were released on Tuesday. While the headline number was stronger than expected, core figures supported the continued yet slow disinflation trend. This presents a dilemma for the Bank of Canada; its target rate is now significantly above current inflation levels, which should be enough to continue to operate downward pressure of inflation, but this is happening at a slower pace than expected. While we don’t think an additional rate increase is warranted, it is not impossible that the central bank decides otherwise at its September 6th meeting.

▪ On the financial markets front, one significant development is the breakout in US Treasury yields, with 10-year government bonds reaching 4.30% on Thursday, a level not seen since last October. Because inflation breakevens have stayed stable through the recent uptick, this should not be seen as markets expecting stickier inflation. It is too early to tell if the upward move in yields is purely flows-driven and temporary or more structural (higher long-term economic growth expectations or an increased risk premium on fiscal sustainability).

▪ After seven months of strength, equity markets seem more hesitant since the beginning of August. Whether we are already there or not, we are getting close to the end of the tightening cycle in North America. Transition periods always come with increased volatility. Markets will be looking for more visibility on the delayed impact of the accumulated tightening that has occurred, but also on what it will take for central bankers to reverse course. Until then, we expect some of the currently observed market rotation to continue and volatility to remain higher. While we remain constructive on markets on the medium to long-term, we have adopted a more defensive stance in most of our strategies over the last few weeks.

ON DECK FOR NEXT WEEK:

▪ Next week’s economic calendar looks relatively light.

▪ We will continue to keep a close eye on the situation in China, the volatility of government bond markets and the evolution of the overall risk sentiment.

For more information, please visit ci.com.

IMPORTANT DISCLAIMERS

This document is provided as a general source of information and should not be considered personal, legal, accounting, tax or investment advice, or construed as an endorsement or recommendation of any entity or security discussed. Every effort has been made to ensure that the material contained in this document is accurate at the time of publication. Market conditions may change which may impact the information contained in this document. All charts and illustrations in this document are for illustrative purposes only. They are not intended to predict or project investment results. Individuals should seek the advice of professionals, as appropriate, regarding any particular investment. Investors should consult their professional advisors prior to implementing any changes to their investment strategies. Certain statements contained in this communication are based in whole or in part on information provided by third parties and CI Global Asset Management has taken reasonable steps to ensure their accuracy. Market conditions may change which may impact the information contained in this document. CI Global Asset Management is a registered business name of CI Investments Inc. © CI Investments Inc. 2023. All rights reserved.