Market Pulse - The week in review - Oct. 20th 2023

Duncan Presant - Oct 24, 2023

The Q3 Business Outlook Survey from the Bank of Canada revealed a significant drop in sentiment, with multiple indicators, such as sales and investment intentions, signalling signs of weakness.

THIS WEEK’S RECAP:

The Q3 Business Outlook Survey from the Bank of Canada revealed a significant drop in sentiment, with multiple indicators, such as sales and investment intentions, signalling signs of weakness. Although labour shortages decreased, there were concerns about persistently high wage expectations particularly in the absence of productivity growth.

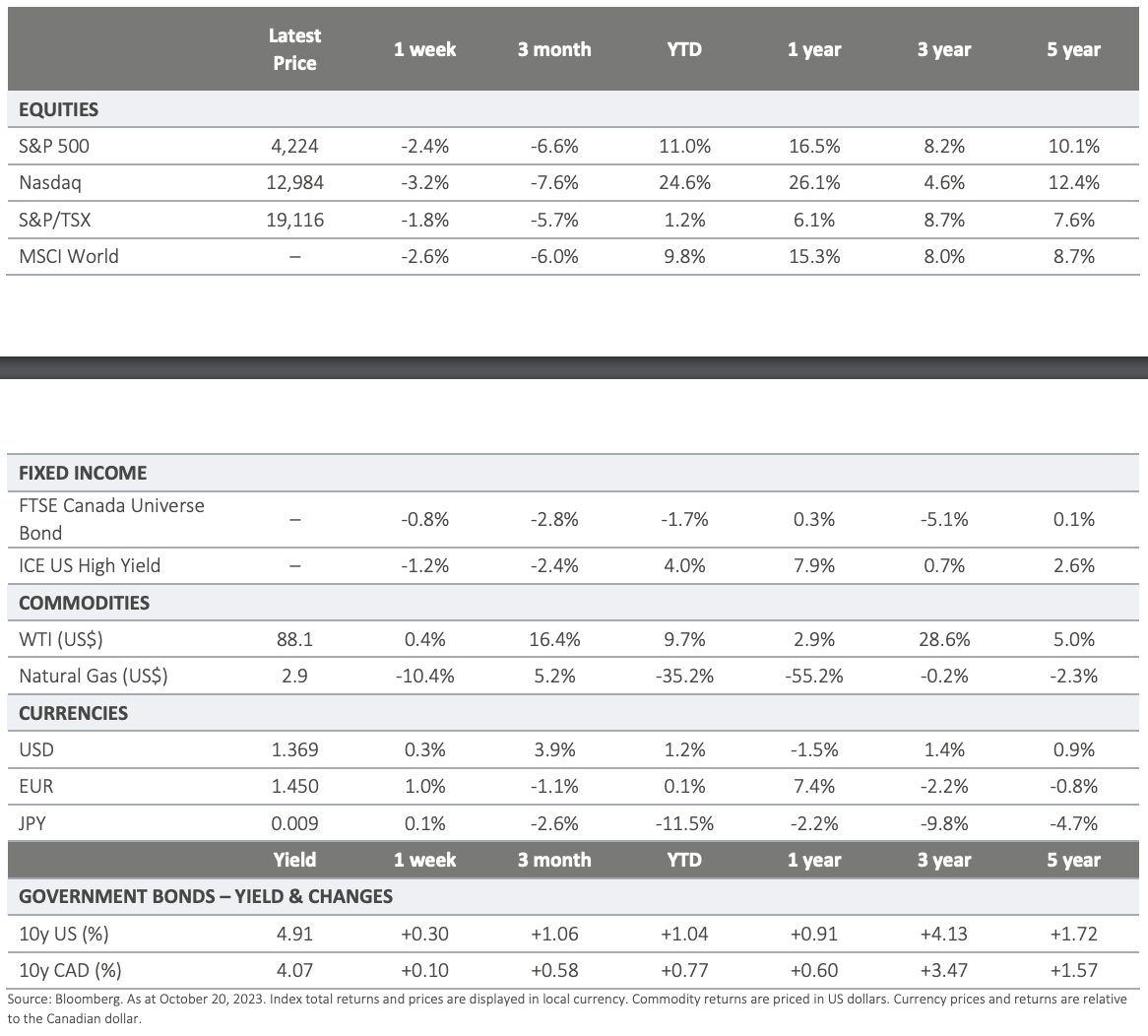

On the inflation front, Canadian CPI for September dropped by 0.1%, lowering the annual rate to 3.8%. Core goods and services inflation decreased though mortgage interest and rental costs remain high. This outcome was an important reversal after a couple months of higher-than-expected inflation prints. This latest read on inflation, combined with a softer Business Outlook Survey and weak economic growth should be enough to keep the Bank of Canada on hold at their upcoming policy-setting meeting on Wednesday (October 25th).

Despite heightened geopolitical risks and the related safe-haven demand seen for US Treasuries and other global bonds last week US yields surged higher again this week spurred by various factors including significantly stronger retail sales data out of US for September. Jerome Powell commented on this upward move in US rates, pointing to unexpected resilience of the US economy and the price discovery process on term premium by which investors are compensated enough to purchase bonds instead of equities or other alternatives.

China's Q3 GDP and September retail sales exceeded expectations, signaling improved growth momentum compared to Q2. Q3 GDP grew by 4.9% year-over-year, while retail sales saw a boost, driven by offline goods and restaurant sales. Despite a smaller-than-expected improvement in fixed asset investment due to property market pressures, there's optimism for Q4 growth, with expectations of continued policy support in response to property challenges and economic uncertainty.

Financial markets were fragile again this week, reacting as one might expect to the unfolding events in the Middle East. Safe-haven assets such as gold and USD both advanced as did oil in response to the conflict tensions. Equities traded sideways over the week, making gains on the back of surprise earnings results, only to be pulled back down by the combination of geopolitical risk, and higher bond yields. The move higher in bond yields was admittedly counterintuitive and may draw in buyers over the coming days and weeks.

ON DECK FOR NEXT WEEK:

Verbiage The Bank of Canada will announce their latest policy rate decision Wednesday. They will also publish revised economic projections by way of their Monetary Policy Report. § The European Central Bank (ECB) is expected to maintain their benchmark rate at their monetary policy meeting on Thursday morning.

Q3 earnings season continues.

For more information, please visit ci.com.

IMPORTANT DISCLAIMERS This document is provided as a general source of information and should not be considered personal, legal, accounting, tax or investment advice, or construed as an endorsement or recommendation of any entity or security discussed. Every effort has been made to ensure that the material contained in this document is accurate at the time of publication. Market conditions may change which may impact the information contained in this document. All charts and illustrations in this document are for illustrative purposes only. They are not intended to predict or project investment results. Individuals should seek the advice of professionals, as appropriate, regarding any particular investment. Investors should consult their professional advisors prior to implementing any changes to their investment strategies. Certain statements contained in this communication are based in whole or in part on information provided by third parties and CI Global Asset Management has taken reasonable steps to ensure their accuracy. Market conditions may change which may impact the information contained in this document. CI Global Asset Management is a registered business name of CI Investments Inc. © CI Investments Inc. 2022. All rights reserved.