Market Pulse - The week in review - Oct. 27th 2023

Duncan Presant - Oct 30, 2023

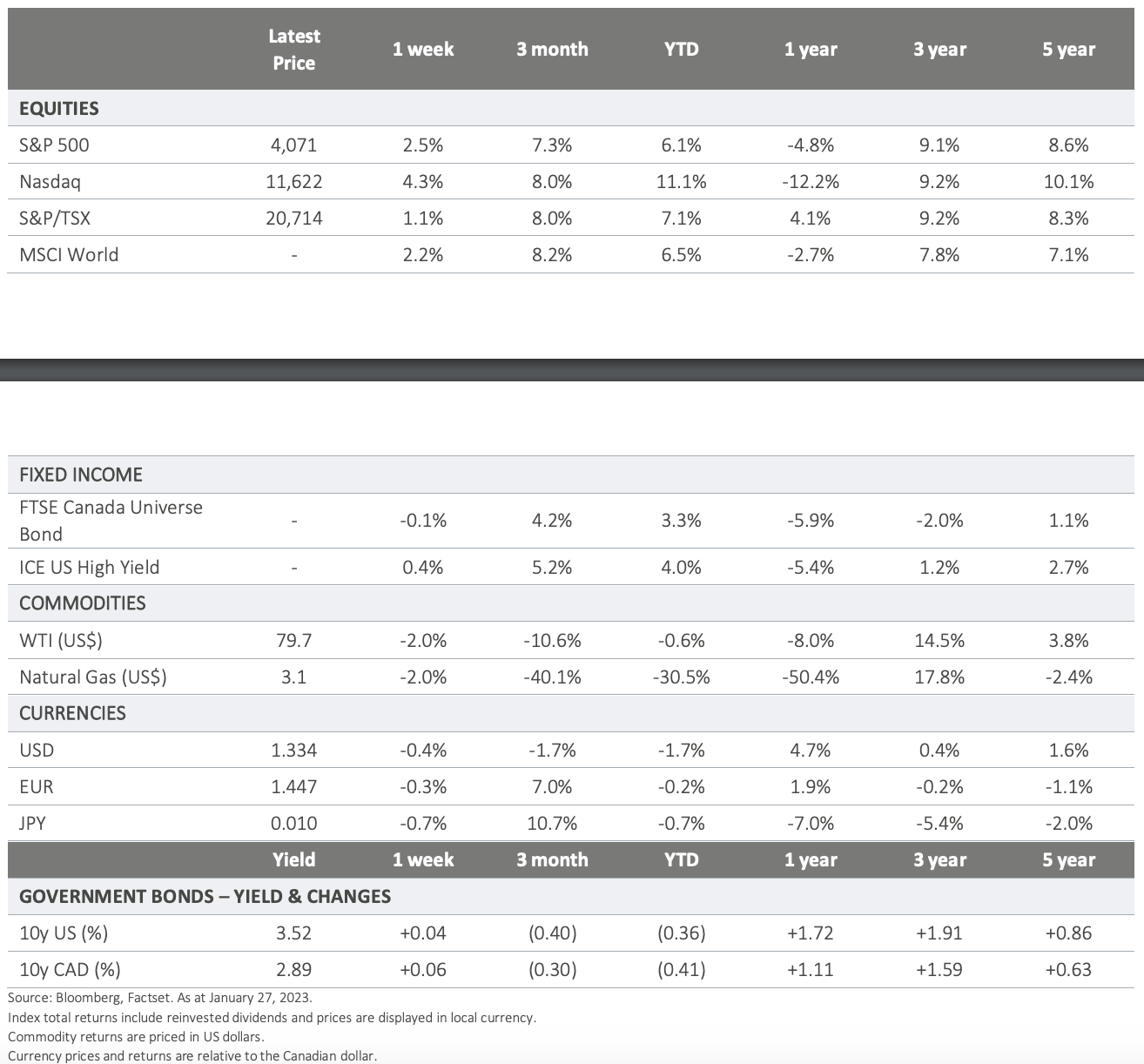

The Bank of Canada held its policy rate at 5% as expected and maintained a hawkish bias in its forward guidance, emphasizing readiness to raise rates further if necessary.

THIS WEEK’S RECAP:

▪ The Bank of Canada held its policy rate at 5% as expected and maintained a hawkish bias in its forward guidance, emphasizing readiness to raise rates further if necessary. Despite concerns about inflation, they noted that several indicators suggest the economy is approaching a supply-demand balance, justifying policy patience. The Bank revised its GDP growth forecast down to 1.2% from 1.8% in July and expects inflation to average 3.0% in 2024, up from the previous 2.5%. The next policy rate adjustment very well could be a cut in mid-2024, contingent on lower inflation, inline with their projections.

▪ The US economy performed exceptionally well in Q3, achieving a 4.9% GDP growth rate. This exceptional performance can be attributed to significant fiscal support, a consumer population less affected by credit conditions, and a tight labor market. While it is widely recognized that the Q3 growth rate is unsustainable (with a consensus forecast of 2.2% for Q4), the more critical question is whether a more significant economic slowdown is on the horizon. Currently, despite weak leading economic indicators, the hard data such as labour, consumption and corporate earnings remains stable. Of particular interest to us is labour data, a key pin in the economic cog, which has yet to show any meaningful signs of decline.

▪ Corporate earnings for Q3 have been mixed so far. Consumer discretionary companies in the travel and leisure services sector had another standout quarter, supported by a resilient US consumer. However, investor sentiment seemed glass half-empty, focusing on the weaker earnings reports. Risk appetite came under considerable pressure, with early signs of a rotation to higher yielding fixed income alternatives.

▪ China delivered another round of stimulus by authorizing a bond issuance of a trillion Yuan (CAD 188 billion), raising their fiscal deficit limit to 3.8% of GDP from 3%. Additionally, China's Foreign Minister visited Washington for discussions with Secretary of State Blinken, potentially paving the way for a significant meeting between President Biden and China's Xi in November at the Asia-Pacific Economic Cooperation Summit in San Francisco. While trade restrictions are not expected to change, improved relations between the two nations would be well-received by the markets.

▪ As expected, the European Central Bank kept its overnight target interest rate unchanged. The ECB is navigating a complex situation, trying to strike a balance between addressing high inflation and a slowing economy. They are cautious about implementing overly tight monetary policy, which could potentially push the economy into a stagflationary downturn. The trajectory of energy prices, a major risk factor for Europe's economic outlook, will play a pivotal role in shaping their policy decisions and the resilience of the economy in coming quarters.

ON DECK FOR NEXT WEEK:

▪ The Federal Reserve will announce their latest policy rate decision Wednesday. Friday will see the release of twinpayroll data, with labour updates coming from both the US and Canada.

▪ Elsewhere, Eurozone Q3 GDP will be released Tuesday. The Bank of Japan will announce changes, if any, to their monetary policy framework midweek as well.

▪ Q3 earnings season continues.

For more information, please visit ci.com.

IMPORTANT DISCLAIMERS

This document is provided as a general source of information and should not be considered personal, legal, accounting, tax or investment advice, or construed as an endorsement or recommendation of any entity or security discussed. Every effort has been made to ensure that the material contained in this document is accurate at the time of publication. Market conditions may change which may impact the information contained in this document. All charts and illustrations in this document are for illustrative purposes only. They are not intended to predict or project investment results. Individuals should seek the advice of professionals, as appropriate, regarding any particular investment. Investors should consult their professional advisors prior to implementing any changes to their investment strategies. Certain statements contained in this communication are based in whole or in part on information provided by third parties and CI Global Asset Management has taken reasonable steps to ensure their accuracy. Market conditions may change which may impact the information contained in this document. CI Global Asset Management is a registered business name of CI Investments Inc. © CI Investments Inc. 2023. All rights reserved.