Market Pulse - The week in review - Nov. 10th

Duncan Presant - Nov 14, 2023

In the Q3 2023 US Senior Loan Officer Opinion Survey (SLOOS), banks tightened lending standards across various loan categories, with consumer lending experiencing the most significant tightening.

THIS WEEK’S RECAP:

In the Q3 2023 US Senior Loan Officer Opinion Survey (SLOOS), banks tightened lending standards across various loan categories, with consumer lending experiencing the most significant tightening. Demand for loans, including residential mortgages and credit cards, declined, signaling potential challenges for consumer spending and a projected sharp slowdown in Q4 GDP growth. Special questions in the SLOOS highlighted tighter lending standards, especially for lower quality borrowers, driven by factors such as an uncertain economic outlook and reduced risk tolerance.

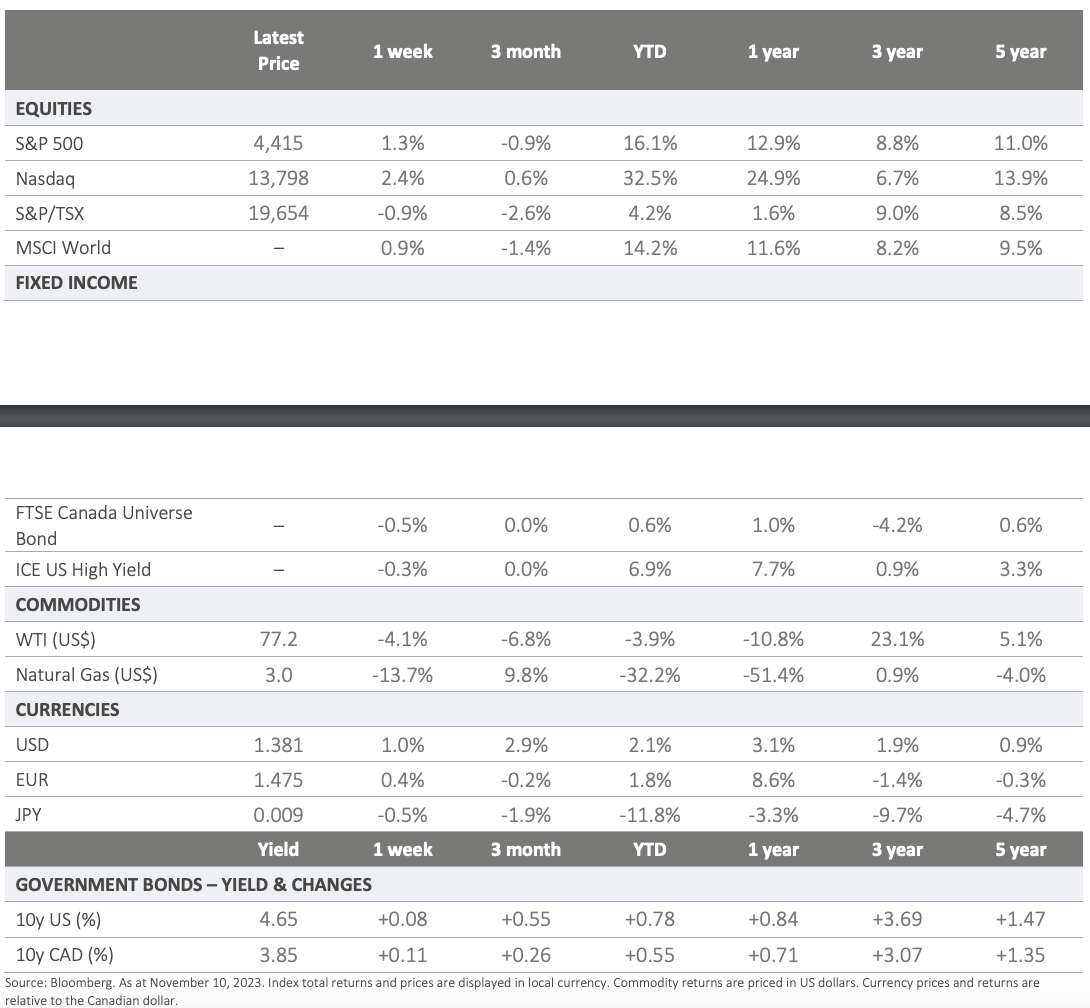

The recent drop in oil prices can be attributed to a combination of factors, including a shift in market sentiment from bullish geo-political risks to bearish macroeconomic concerns. Factors including a worsening oil demand outlook in China, increased oil supply, weak US economic data, technical weaknesses in the market, and a rise in producer selling have all contributed to the decline in oil prices.

Manufacturing and service sector indicators from Europe and the UK are signaling a persistent slowdown in business activity, with the manufacturing sector feeling the brunt of it. This downturn is echoed in China's export figures, which have declined for the seventh consecutive month, highlighting a protracted global decrease in demand for goods. § Australia's central bank, the Reserve Bank of Australia, opted for a dovish (cautious) rate hike, raising the cash target rate by 25 bps to 4.35%. They have taken a measured stance, similar to Canada, due to persistently high inflation and the potential impact on real incomes in an economy experiencing below-trend growth.

The US Presidential election is upon us, promising a year filled with political theatrics. Trump and Biden are currently in a tight race, each polling at about 45%. Amidst the spectacle, fleeting and unsubstantiated media narratives will intermittently ratchet up market volatility, while the crucial issues of the fiscal landscape are likely to be overshadowed in the commotion.

ON DECK FOR NEXT WEEK: Canadian banks will be closed Monday in observation of Remembrance Day. Stock markets remain open, bond market will be closed. The US will release October updates on CPI (Wednesday) and Retail Sales (Thursday) with both expected to come in considerably lower than September.

For more information, please visit ci.com.

IMPORTANT DISCLAIMERS

This document is provided as a general source of information and should not be considered personal, legal, accounting, tax or investment advice, or construed as an endorsement or recommendation of any entity or security discussed. Every effort has been made to ensure that the material contained in this document is accurate at the time of publication. Market conditions may change which may impact the information contained in this document. All charts and illustrations in this document are for illustrative purposes only. They are not intended to predict or project investment results. Individuals should seek the advice of professionals, as appropriate, regarding any particular investment. Investors should consult their professional advisors prior to implementing any changes to their investment strategies. Certain statements contained in this communication are based in whole or in part on information provided by third parties and CI Global Asset Management has taken reasonable steps to ensure their accuracy. Market conditions may change which may impact the information contained in this document. CI Global Asset Management is a registered business name of CI Investments Inc. © CI Investments Inc. 2023. All rights reserved.