[Winter 2026 GPS] The US: Still the Land of Unpredictability

James Schofield - Mar 27, 2026

In last year's newsletters we indicated that the Trump Administration's trade and foreign policies would engender a climate of unpredictability for financial markets until term ends in 2029. Unfortunately we've been correct so far!

In our 2025 spring newsletter, we noted that the new US administration, with its trade policy and the geopolitical risks it brings, makes the US a land of unpredictability, which creates instability for businesses and financial markets. Later, in the summer of 2025 newsletter, we indicated that the unpredictability will remain with us until 2029. Unfortunately, it seems we are correct so far!

Tariffs: here we go again

In February 2026, the US Supreme Court ruled that all the broad-based tariffs imposed by the US president under the “International Emergency Economic Powers Act (IEEPA)” were unlawful, without indicating what would happen to the billions of dollars already collected, opening the door to possibly years of legal suits against the administration by companies trying to get tariffs refunded.

The US president issued a new executive order imposing a 10% tariff globally for 150 days (imposing Section 122 of the 1974 Trade Act) and later increased it to 15%. He plans, at least until now, to continue imposing tariffs using another section of the 1974 Trade Act after 150 days.

Several countries that reached agreements with the US before the Supreme Court decision may now want to renegotiate for a better deal, making the situation increasingly unpredictable.

Greenland, Venezuela, Cuba, Iran

In January 2026, a significant diplomatic, economic, and geopolitical dispute had arisen between the U.S. administration and European allies, particularly Denmark, in response to President Trump's intention to acquire Greenland. Trump maintains that Greenland is essential for U.S. security and for critical minerals, and he has threatened to impose 25% tariffs on EU products if allies oppose the acquisition. This issue seemed to have settled for now, but it rattled the global markets for a few days.

After Greenland, Venezuela and Cuba were next in line. Finally, on February 28th, 2026, the US and Israel started a military campaign against Iran, which, as we are writing this part, caused the oil price to soar past $100 a barrel.

Naturally, the attack on Iran increased geopolitical risk and short-term market volatility. Energy prices surged, investors flocked to safe-haven assets such as gold & USD, and Asian markets and currencies declined sharply.

The Strait of Hormuz remains a critical chokepoint, with nearly 20% of global oil passing through this corridor. From a macroeconomic and portfolio perspective, the main concern is not temporary price swings but whether higher energy costs become persistent enough to impact inflation and growth forecasts.

The significant U.S. naval presence and the incentives faced by producers and consumers suggest that a prolonged disruption is unlikely. The US and regional allies have the capacity and motivation to keep shipping lanes open. In addition, OPEC+ has responded, albeit modestly, by increasing its supply, and the G7 countries announced that they could tap into their oil reserves. Consequently, second-order effects on inflation and economic activity are a downside risk rather than as part of the baseline scenario, at least for now.

A prolonged period of oil above $100 a barrel will boost global inflation, reducing the odds of central banks cutting interest rates. In addition, and more importantly, a prolonged high oil price will reduce the GDP of many Asian economies that depend heavily on oil imports.

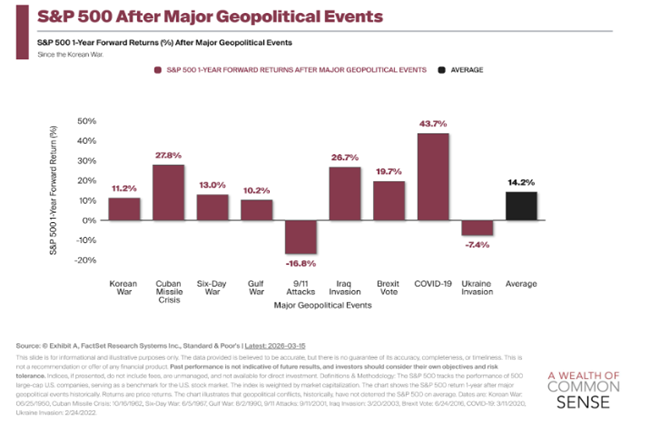

We do not know how long oil will remain at $100 per barrel, or whether it will go higher, but for investors, the focus should be on how these events influence portfolio risk rather than on immediate market movements. Although volatility in energy and broader risk assets may continue in the near term, history shows that, in similar scenarios, these energy price spikes tend to be short-lived and do not warrant changing long-term asset allocation decisions.

US economy:

In our 2025 summer newsletter, we indicated that the US economy is sending mixed signals, as corporate earnings, especially for mega-cap technology companies such as NVIDIA, continue to grow at an impressive pace, while the labour market is showing signs of weakening.

NVIDIA, for example, reported record-breaking results on February 25, 2026—revenue of $68.1 billion (+73% YoY). However, the February 2026 US jobs report points to a cooler, but not collapsing, labour market. In February, the U.S. economy unexpectedly lost about 92,000 jobs, and the unemployment rate rose to 4.4%, signalling that hiring momentum had slowed. February's job losses were widespread, affecting factories, construction firms, and the federal government, all of which reduced their workforce. Even the healthcare sector, which has been a strong point in the job market, lost 28,000 jobs in February — partly due to a nurses' strike. At the same time, wage growth remains solid at roughly 3.8% year over year, still outpacing current inflation.

For markets, this combination of higher unemployment with higher-than-normal wage growth suggests the Federal Reserve can remain patient and keep interest rates level for now, with any eventual rate cuts likely to be gradual. The data points to a slower growth trend rather than a sharp downturn, which tends to create periods of volatility as investors reassess earnings and interest‑rate expectations.

We must acknowledge that, despite all the risk factors surrounding the U.S. economy, and the “Sell America” trade gaining momentum again lately, the US economy remains the largest and most diversified in the world. The US market is by far the most liquid and transparent globally. The US has some of the world's most innovative companies generating billions of dollars in free cash flow annually. Over the last two years, the largest U.S. technology companies saw their stock prices surge to levels that raised questions about whether or not we are in an AI bubble. These companies are spending billions in their race to achieve AI leadership. That level of investment raises questions about whether it will eventually deliver a worthwhile return. The AI bubble, CapEx, and disruption will be topics we cover in detail in our next GPS.