Market Pulse - The week in review

Duncan Presant - Dec 21, 2022

The US November CPI data confirmed that prices are finally rolling over. At 7.1%, inflation is well below June’s peak of 9%, but is still too high for central banks to lower their guard.

THIS WEEK’S RECAP:

▪ The US November CPI data confirmed that prices are finally rolling over. At 7.1%, inflation is well below June’s peak of 9%, but is still too high for central banks to lower their guard. While prices for goods continue to drop, the services, rents and labour cost components remain the barrier to a more significant step down in inflation. These components are the most affected by transmission lags, so we expect the fall in inflation to continue and probably even accelerate. Where inflation lands remains an open and crucial question.

▪ Another factor that confirms the downward pressures on inflation comes from a broad downturn in household consumption across developed economies. This shows consumers have begun to adjust spending behaviours in response to higher interest rates.

▪ In his final speech of the year, Bank of Canada Governor Macklem remained unwavering: the objectives of taming inflation and achieving long-term price stability remain crucial, even if at the cost of an economic slowdown. While the Bank said it will be data-driven in assessing whether any further rate hikes are required, no further increases are expected by markets, and they begun to build in the possibility for a first rate drop in late 2023.

▪ This week was filled with central bank policy announcements. The Federal Reserve delivered on expectations with a 50 basis point (bps) increase, taking their target rate up to 4.25%. The statement supporting the decision as well as Powell’s press conference were received as more hawkish than expectations, especially following Tuesday’s rather soft inflation numbers. European, UK, Swiss, Norway and Taiwanese central banks also raised their overnight target rates by either 25 or 50 bps.

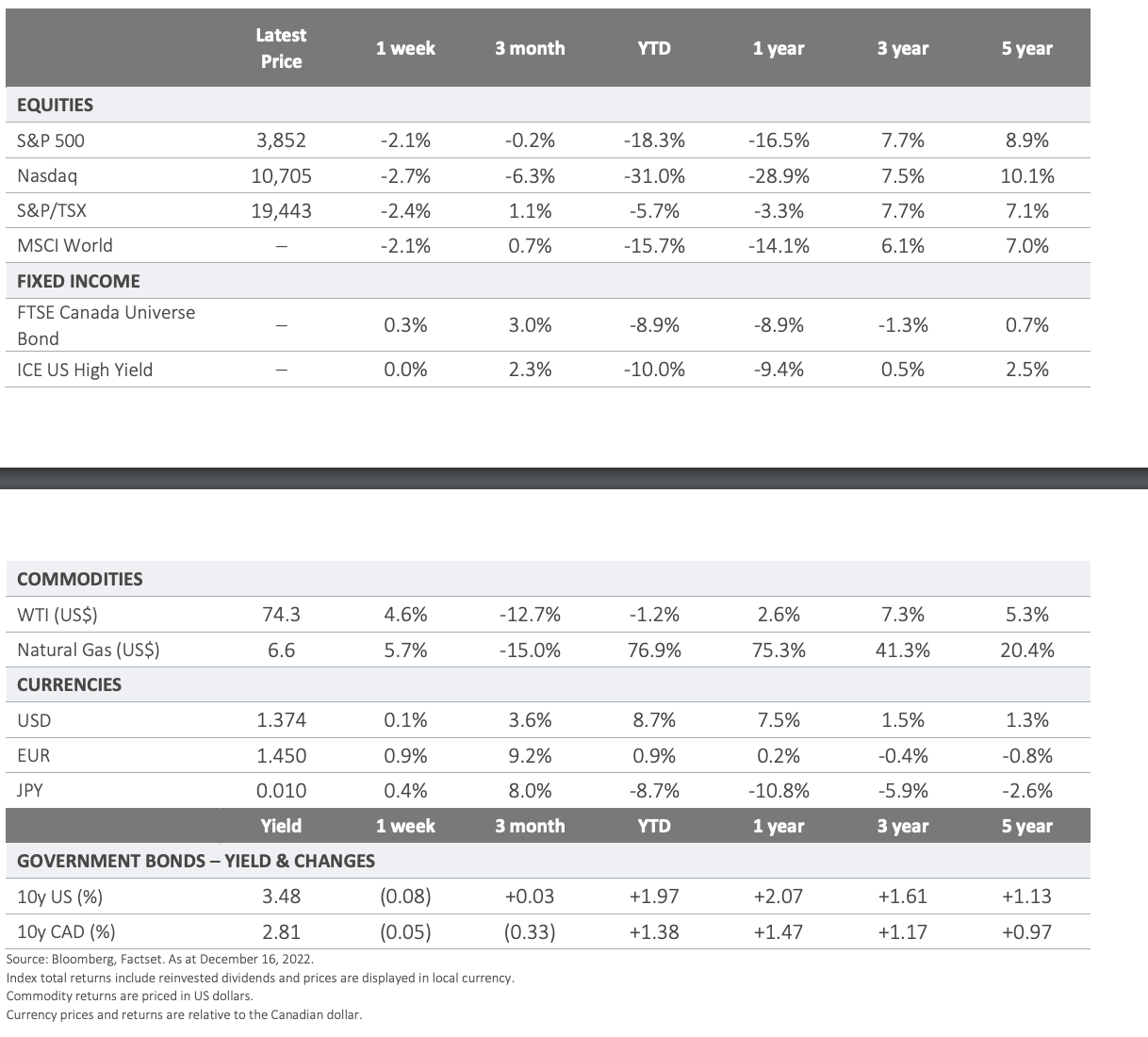

▪ The joint hawkishness of central banks spoiled the post-CPI rally in risky assets, dampening the market enthusiasm as we enter the last few weeks of what has been a difficult year. Like last week, global equity markets finished the week down a few percentage points. Latest Price 1 week 3 month YTD 1 year 3 year

ON DECK FOR NEXT WEEK:

ON DECK FOR NEXT WEEK:

▪ It will be quieter on the data front as markets ease into the Holidays. On Wednesday, Canadian CPI will be released, and we expect to see some improvement driven by similar themes seen last week in US and UK data: reduced household demand as well as lower food and energy prices.