Market Pulse - The week in review - July 28th 2023

Duncan Presant - Aug 02, 2023

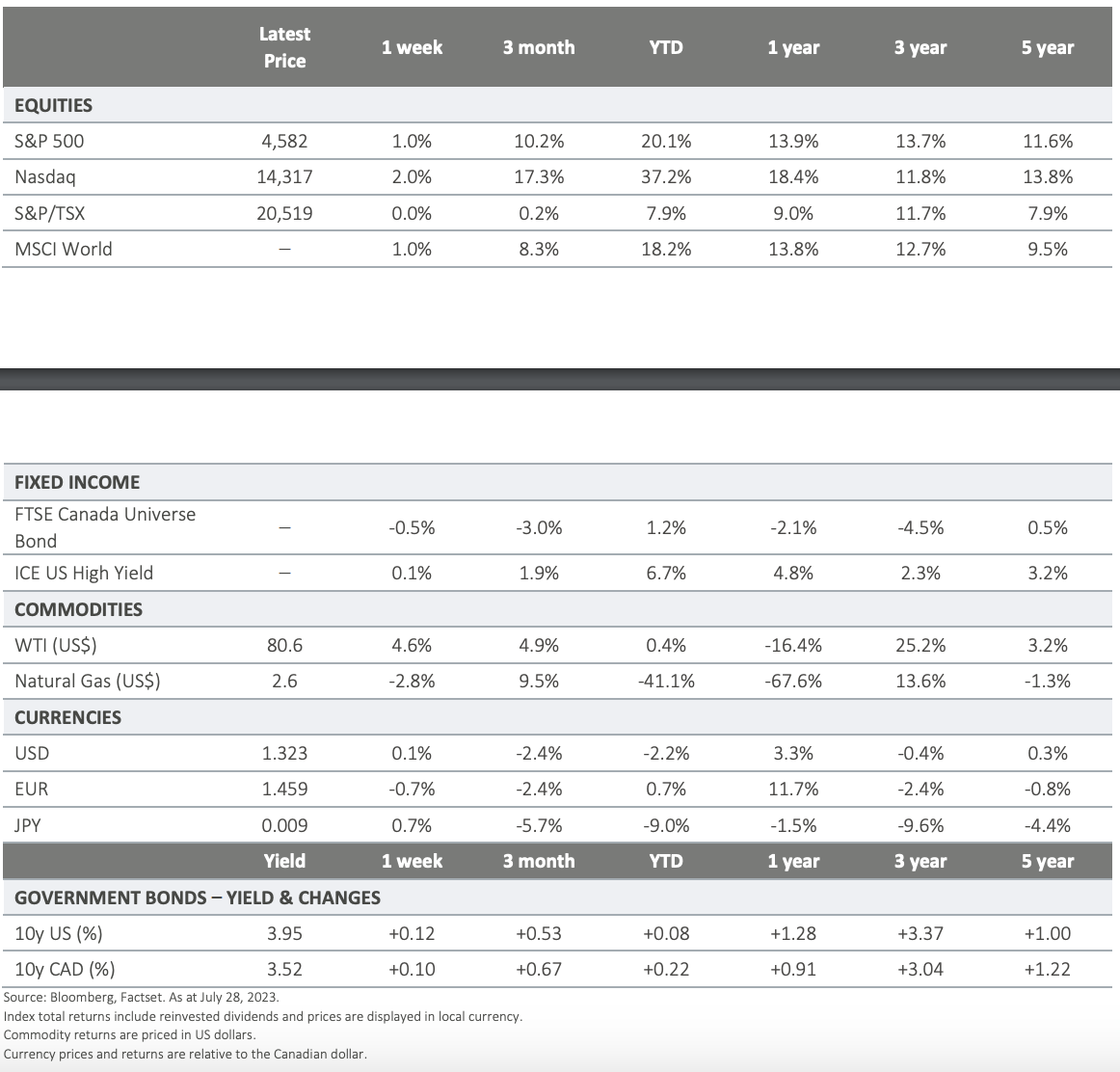

As anticipated, both the US and Europe increased their target interest rates by 25 bps, reaching 5.25% and 3.75%, respectively.

THIS WEEK’S RECAP:

▪ As anticipated, both the US and Europe increased their target interest rates by 25 bps, reaching 5.25% and 3.75%, respectively. Central bankers have shifted away from a full-out tightening bias and the use of forward guidance to signal rate hikes. Instead, they are now closely monitoring intra-meeting data and are prepared to respond with further rate increases or pause based on the trajectory of inflation.

▪ The Bank of Japan made a long-awaited adjustment to their Yield Curve Control (YCC) targets, effectively moving the cap on the 10yr Japan Government Bond (JGB) from 0.5% to 1%. The next shoe to drop would be a move away from negative overnight rates (NIRP), their overnight target rate remains -0.1%. These changes have the potential to nudge global yields higher as Japanese yields become marginally more attractive to domestic investors.

▪ Economic activity is proving to be more resilient than expected in the US. The advanced Q2 GDP reading was +2.4%, much stronger than widely expected. Higher borrowing costs failed to slow the economy. There is some concern that rates will need to be raised even further to cool consumption.

▪ Tighter credit conditions have arrived in Europe. A quarterly survey of lenders showed a strong decline in demand for loans by firms, driven by rising interest rates and declining fixed investment. Household demand for mortgages did improve slightly, while overall lending standards across banks have generally tightened. ECB President, Christine Lagarde, reiterated that financing conditions are increasingly dampening demand, this after raising interest rates from -0.5% to +3.25% over the past 12 months.

▪ China’s government held its Politburo meetings early in the week, an opportunity to reset or highlight any adjustments to policy priorities. Measures will be taken to boost consumption, encourage government investment, stabilize foreign trade, and support the development of strategic emerging industries, especially in the digital economy. Rules around property ownership (lending parameters) may be eased as well.

▪ Equities are holding onto recent gains despite a mixed earnings season thus far. Q2 earnings growth is in the low singledigits, while sales remain robust for the most part. In very broad terms, this dynamic suggests margin erosion relative to past quarters, and could be a precursor for a slowdown on the business investment front and has the potential to weigh on economic activity (a warning signal for employment).

ON DECK FOR NEXT WEEK:

• The Bank of England is expected to raise rates again on Thursday, with a 25-50 bp hike expected. The latest read on Canadian and US employment comes Friday. As counterintuitive as it may sound, both central banks are desperate to see some softening in the labour market.

• US earnings season continues.

For more information, please visit ci.com.

IMPORTANT DISCLAIMERS This document is provided as a general source of information and should not be considered personal, legal, accounting, tax or investment advice, or construed as an endorsement or recommendation of any entity or security discussed. Every effort has been made to ensure that the material contained in this document is accurate at the time of publication. Market conditions may change which may impact the information contained in this document. All charts and illustrations in this document are for illustrative purposes only. They are not intended to predict or project investment results. Individuals should seek the advice of professionals, as appropriate, regarding any particular investment. Investors should consult their professional advisors prior to implementing any changes to their investment strategies. Certain statements contained in this communication are based in whole or in part on information provided by third parties and CI Global Asset Management has taken reasonable steps to ensure their accuracy. Market conditions may change which may impact the information contained in this document. CI Global Asset Management is a registered business name of CI Investments Inc. © CI Investments Inc. 2023. All rights reserved.