Market Pulse - The week in review - Sept. 11th

Duncan Presant - Sep 11, 2023

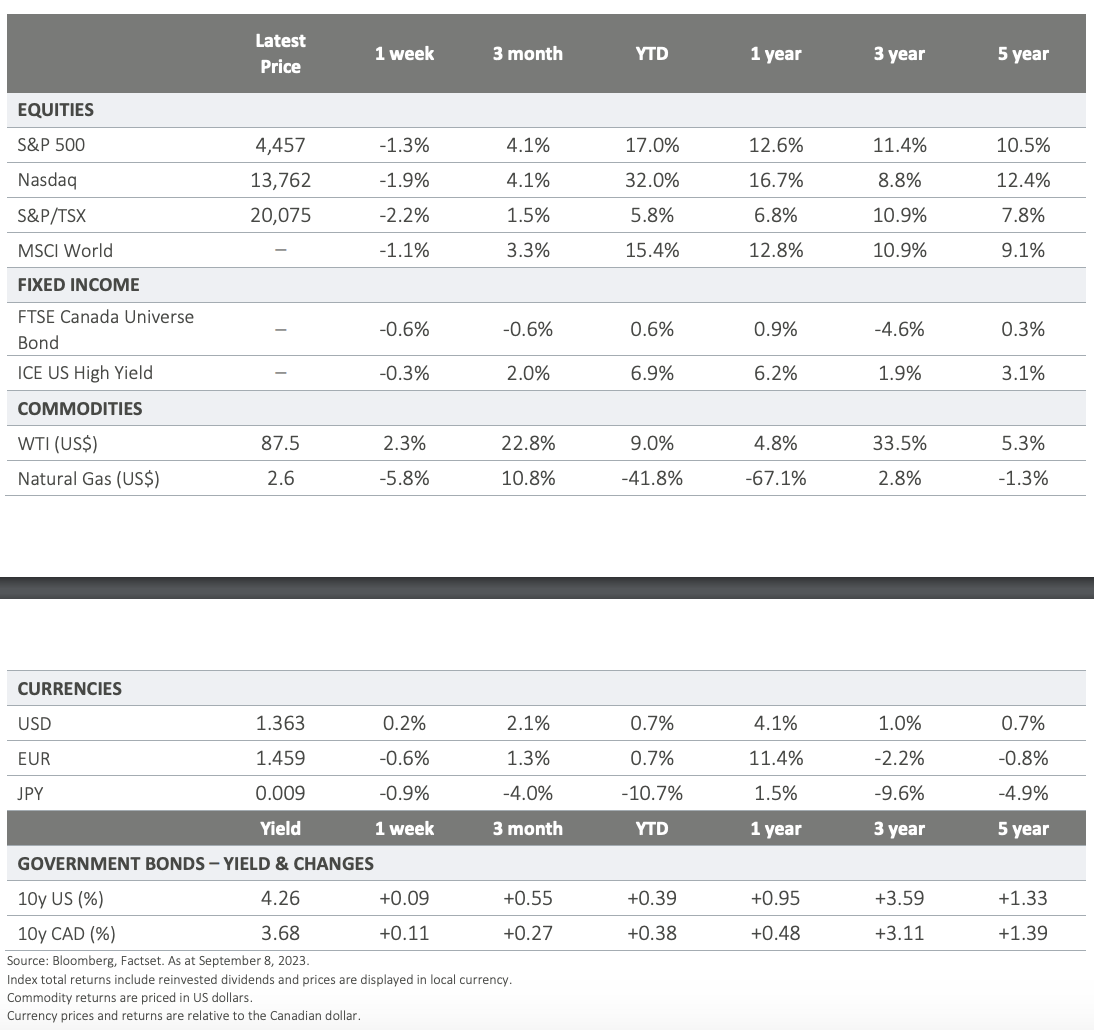

The Bank of Canada opted to maintain its overnight interest rate at the current level of 5%. They acknowledged a deceleration in the economy, a trend deemed essential to alleviate inflationary pressures.

THIS WEEK’S RECAP:

▪ The Bank of Canada opted to maintain its overnight interest rate at the current level of 5%. They acknowledged a deceleration in the economy, a trend deemed essential to alleviate inflationary pressures. They pointed to a softening labor market and a substantial reduction in excess demand as confirmation of this slowdown. Nevertheless, the bank continues to express significant concerns regarding inflation, which sits above 3%, well above their 2% mandated target. As a result, the possibility of further rate hikes remains on the table, should it become necessary.

▪ Monthly employment jumped in Canada in August, though the unemployment rate was unchanged at 5.5%. The highly volatile Labour Force Survey reported an increase of 40,000 jobs against population growth of 103,000. The Bank of Canada will be comforted by the slight drop in wage growth, though they will need to see a more material and sustained downturn in labour data before completely abandoning the notion of future rate hikes.

▪ Various US manufacturing and service activity indicators continue to highlight a resilient economy. To this end, a running estimate of Q3 GDP by the Federal Reserve Bank of Atlanta is tracking above 5%. As the tight labour market begins to normalize, and with the backdrop of high interest rates we do expect this economic outperformance to slowdown in coming months. Meanwhile, the US dollar is rallying on the twin tailwinds of relative economic strength and elevated yields.

▪ Oil (Brent crude) surpassed $90 a barrel, marking the first time it has reached this level in over a year. Saudi Arabia and Russia have both confirmed their commitment to maintaining output restrictions through the end of 2023. Saudi Arabia is managing its supply at approximately 9 million barrels per day, which is 25% below its officially declared maximum production capacity. Although this approach is supporting oil prices at the moment, the spare production capacity should act as a buffer in the event of increased demand, which in turn should limit prices and avoid the price shock experienced in early 2022.

ON DECK FOR NEXT WEEK:

▪ In anticipation of the Federal Reserve’s next rate policy decision (Sept 20), all eyes will be on Wednesday’s US CPI release for August.

▪ Thursday morning the European Central Bank will share their latest monetary policy update. We expect a 25 bp hike, with a slightly less aggressive tone on the future path of rates.

For more information, please visit ci.com.

IMPORTANT DISCLAIMERS

This document is provided as a general source of information and should not be considered personal, legal, accounting, tax or investment advice, or construed as an endorsement or recommendation of any entity or security discussed. Every effort has been made to ensure that the material contained in this document is accurate at the time of publication. Market conditions may change which may impact the information contained in this document. All charts and illustrations in this document are for illustrative purposes only. They are not intended to predict or project investment results. Individuals should seek the advice of professionals, as appropriate, regarding any particular investment. Investors should consult their professional advisors prior to implementing any changes to their investment strategies. Certain statements contained in this communication are based in whole or in part on information provided by third parties andCI Global Asset Management has taken reasonable steps to ensure their accuracy. Market conditions may change which may impact the information contained in this document. CI Global Asset Management is a registered business name of CI Investments Inc. © CI Investments Inc. 2023. All rights reserved.