ETF Taxation: CRA Foreign Asset Disclosure and U.S. Estate Tax

Duncan Presant - Nov 01, 2023

The purpose of this reporting is to allow the CRA to better track and address compliance risks, and to help combat international tax evasion and aggressive tax avoidance.

The CRA requires Canadian resident taxpayers (individuals, corporations and certain partnerships and trusts) to file form T1135, Foreign Income Verification Statement, if the total cost of their specified foreign properties (SFP) exceeds $100,000 (in Canadian dollars) at any time during the year. Cost is generally defined as the adjusted cost base of the properties. The purpose of this reporting is to allow the CRA to better track and address compliance risks, and to help combat international tax evasion and aggressive tax avoidance. Information to be reported on the form includes:

- The type of foreign assets held;

- The location of the assets (by country);

- The cost amount of the assets (maximum during the year and amount at year-end);

- The amount of any income earned by the foreign assets in the year, including any capital gain/loss on the disposition of the assets.

The form must be filed on or before the due date of the taxpayer’s income tax return. Failure to file may result in penalties of $25 per day (to a maximum of $2,500) with additional penalties in cases of gross negligence.

What is specified foreign property?

- SFP generally includes (but is not limited to):

- Funds situated, deposited or held outside Canada

- Land or real property (other than personal-use property) situated outside Canada

- Shares of foreign corporations

- Shares of corporations resident in Canada but held outside Canada

- An interest in a non-resident trust that was acquired for consideration

- A debt owed by a non-resident, including government and corporate bonds, debentures, mortgages and notes receivable

- An interest in a foreign insurance policy

- Precious metals, gold certificates and futures contracts held outside Canada

SFP does not include:

- SFP held within Canadian mutual funds or ETFs (trusts or corporations)

- Personal-use real property (e.g., vacation property)

- SFP held within certain registered plans, including RRSPs, RRIFs, RESPs, RDSPs and TFSAs

- Property used exclusively in carrying on an active business

Since most Canadian ETFs are mutual funds for tax purposes, they do not need to file Form T1135 in respect of their foreign holdings. Similarly, because Canadian ETFs are not considered SFP, investors in Canadian ETFs don’t need to report this investment on the form, even if the ETF invests in foreign securities. For Canadians, as a benefit of purchasing Canadian-listed ETFs versus U.S.-listed ETFs or foreign securities directly, this can mean simplified tax reporting. Here’s an example to illustrate the potential difference in reporting requirements:

Latoya, a Canadian resident, purchased ABC’s US Total Market ETF, which is a U.S.-listed ETF, for $75,000 (CAD) earlier this year. She also invested $30,000 (CAD) in a deposit account in the United States.

Because Latoya’s U.S. ETF and U.S. deposit are specified foreign properties with a total cost in excess of $100,000 (CAD), she is required to file form T1135 for the year, and each subsequent year she continues to hold the properties with a cost amount in excess of $100,000. Included on the form, Latoya would need to indicate the type of foreign properties held and gross income from (and any gains from the disposition of) the properties. This would be in addition to her income tax return for the year. Failure to file the form could result in penalties of $25 per day to a maximum of $2,500.

Leslie, also a Canadian resident, purchased $75,000 (CAD) of DEF’s US Exposure Market ETF, which is a Canadian-listed ETF with exposure to the U.S. market, this year. At the same time, she purchased $30,000 (CAD) of DEF’s High Interest Savings ETF.

Leslie is not required to file form T1135 as her investments are not considered specified foreign properties for these purposes.

U.S. estate tax considerations1

Under Canadian tax rules, individuals are deemed to have disposed of their assets at the time of death. This often results in income or capital gains for the year of death and a related tax liability for which the deceased’s estate is liable. United States tax rules, however, do not apply a deemed disposition at death – instead, the U.S. charges an estate tax applied at graduated rates based on the fair market value of an individual’s estate at death.

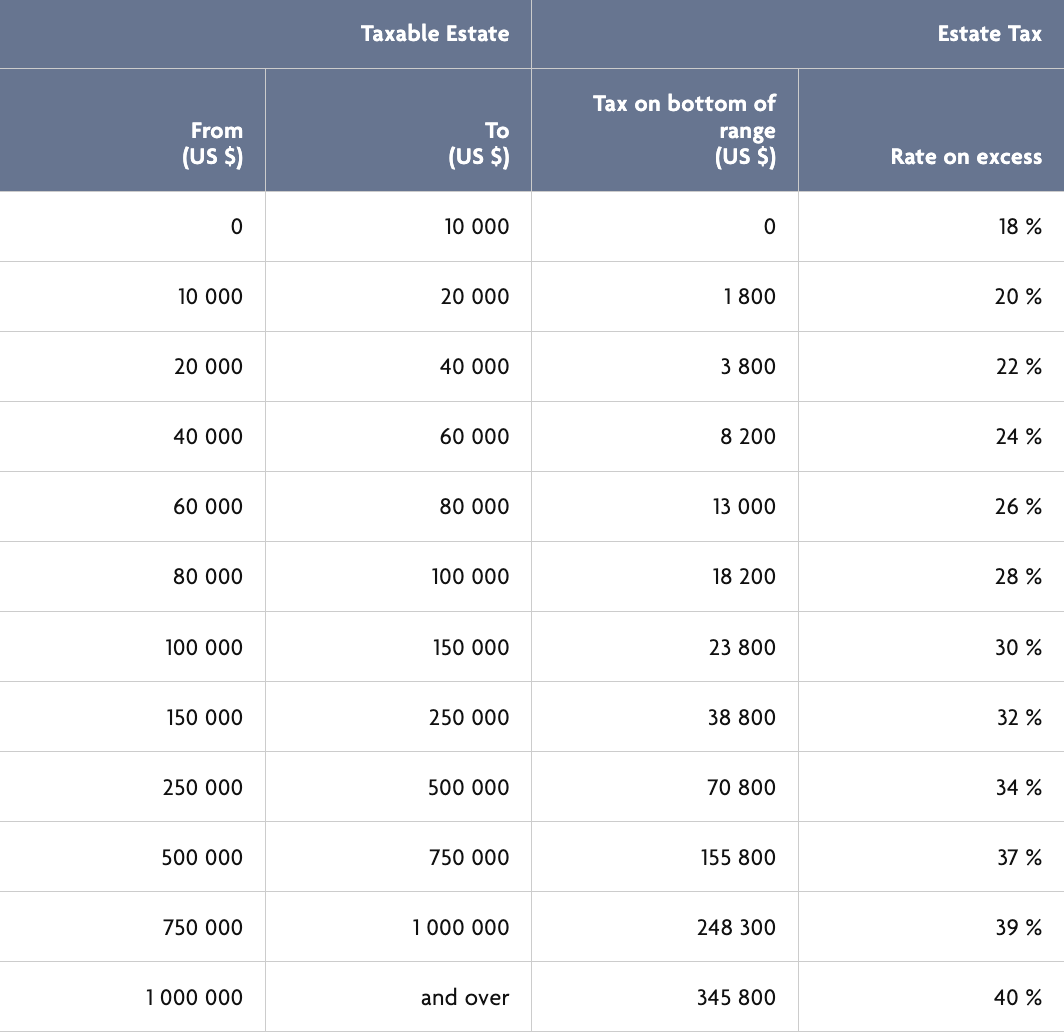

The U.S. estate tax normally applies to both U.S. persons (based on their worldwide estate) and non-U.S. persons (based on U.S. situs property). U.S. persons normally include U.S. residents, Green Card holders and U.S. citizens regardless of where they reside. The following table shows graduated U.S. estate tax rates for 2023.

Certain deductions and credits can be used to reduce or eliminate a U.S. estate tax liability (including a marital deduction and credit for couples). One of the most significant credits for U.S. persons is a unified credit that, for 2023, eliminates U.S. estate taxes for taxable estates of up to $12.92 million USD. Canadian residents who are not U.S. persons are entitled to the same unified credit as U.S. persons, but it’s prorated based on the value of U.S. situs assets versus worldwide assets at the time of death. In other words, for both U.S. persons and Canadians who are not U.S. persons, U.S. estate taxes may apply where the value of their estate exceeds $12.92 million USD (2023) at the time of death. Also, for Canadians, a U.S. estate tax return is normally required where U.S. situs property exceeds $60,000 USD, even though the estate might not be subject to estate taxes given to the $12.92 million USD prorated exemption. Where required, the return is normally due nine months after the date of death, with penalties applied for non-compliance.

What is U.S. “situs” property for U.S. estate tax purposes?

For non-U.S. persons, the U.S. estate tax applies only to U.S. situs property, which is property that’s situated in the U.S. It includes:

- Real property situated in the U.S.

- U.S. securities held inside or outside of Canada

- Certain U.S. debt obligations

- U.S. mutual funds and ETFs

- U.S. situs properties held in registered plans

- Interests in U.S. retirement plans or annuities including different types of IRA and 401(k) plans

- Business assets used in a U.S. business

The following are generally excluded from the U.S. estate tax calculation for non-U.S. persons:

- U.S. bank deposits

- U.S. T-bills

- U.S. life insurance policies

- Canadian mutual funds and ETFs

Canadian ETFs can be an effective way for Canadians who are not U.S. persons to have exposure to U.S. markets without a potential U.S. estate tax liability. While U.S. securities, including U.S. ETFs, are U.S. situs properties subject to U.S. estate taxes, Canadian mutual funds, including Canadian ETFs, avoid this liability. Let’s look at a compelling example:

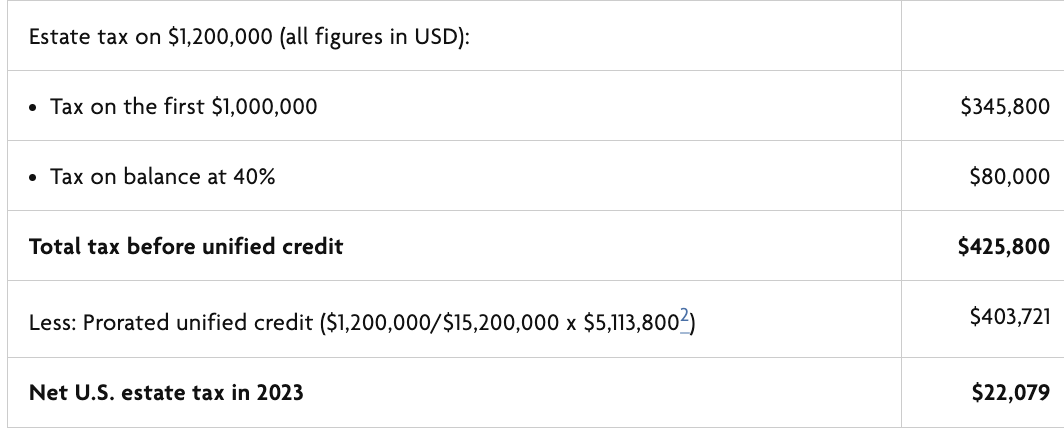

Emily, an unmarried Canadian, died in 2023. At the time of death, she owned a portfolio of U.S. ETFs and U.S. stock worth $1.2 million USD, and non-U.S. situs assets worth $14 million USD, for a total estate of $15.2 million USD. Emily’s net U.S. estate tax would be calculated as follows:

If, on the other hand, Emily’s exposure to U.S. assets was achieved through Canadian ETFs, she would not have a U.S. estate tax bill for her year of death, nor would her estate need to file a U.S. estate tax return on her behalf. These two hypothetical situations illustrate the contrast in tax obligations and provides food for thought when Canadian individuals are seeking exposure to U.S.-related assets.

1 Comments refer to U.S. federal estate taxes. Estate taxes at the state level, if any, are beyond the scope of this article.

2 Credit amount that exempts a $12.92 million USD estate from U.S. estate tax.

Wilmot George Jr., CFP, TEP, CLU, CHS

Vice-President

Tax, Retirement and Estate Planning

Throughout his career, Wilmot has held progressive positions in the areas of tax and estate planning, financial planning, banking, and securities analysis. He has completed numerous courses related to taxation, securities and mutual fund investing, insurance and estate planning. Wilmot received his Bachelor of Arts Degree (with Honours) in Mathematics for Commerce from York University. He also holds the Certified Financial Planner (CFP), Trust and Estate Practitioner (TEP), Chartered Life Underwriter (CLU) and Certified Health Insurance Specialist (CHS) designations. Since 2001, Wilmot has spent his time guiding financial advisors on tax and estate planning matters through presentations, one-on-one consulting and written communication.He has been featured in various financial forums including The Globe and Mail, The National Post, Advisor.ca, and Investment Executive. Additionally, Wilmot has delivered presentations for The Financial Advisors Association of Canada (Advocis), the Society of Trust and Estate Practitioners (STEP) and The Institute of Advanced Financial Planners (IAFP). Away from work, Wilmot enjoys various sports, traveling and spending time with family and friends.

IMPORTANT DISCLAIMER

This communication is published by CI Global Asset Management (“CI GAM”). Any commentaries and information contained in this communication are provided as a general source of information and should not be considered personal investment advice. Facts and data provided by CI GAM and other sources are believed to be reliable as at the date of publication.

Certain statements contained in this communication are based in whole or in part on information provided by third parties and CI GAM has taken reasonable steps to ensure their accuracy. Market conditions may change which may impact the information contained in this document.

Information in this communication is not intended to provide legal, accounting, investment or tax advice, and should not be relied upon in that regard. Professional advisors should be consulted prior to acting based on the information contained in this communication.

You may not modify, copy, reproduce, publish, upload, post, transmit, distribute, or commercially exploit in any way any content included in this communication. You may download this communication for your activities as a financial advisor provided you keep intact all copyright and other proprietary notices. Unauthorized downloading, re-transmission, storage in any medium, copying, redistribution, or republication for any purpose is strictly prohibited without the written permission of CI GAM.

CI Global Asset Management is a registered business name of CI Investments Inc.