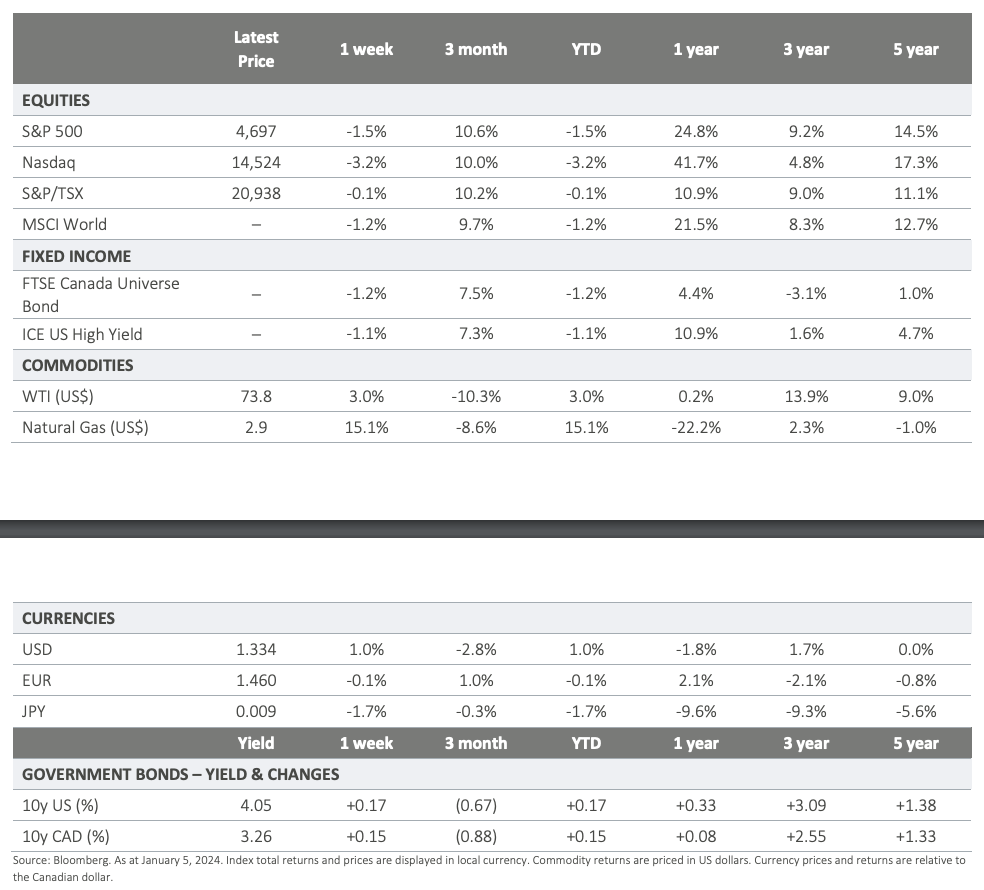

Market Pulse - The week in review - Jan. 8th 2024

Duncan Presant - Jan 08, 2024

Canada experienced flat job growth in December, maintaining an unemployment rate of 5.8% and recording a slight increase in hourly wages to 5.7%.

THIS WEEK’S RECAP:

Canada experienced flat job growth in December, maintaining an unemployment rate of 5.8% and recording a slight increase in hourly wages to 5.7%. Meanwhile, the US saw stronger-than-expected job creation, reducing its unemployment rate to 3.7%. Given that wage increases generally lag behind overall inflation, a slowdown in wage growth is anticipated in the coming months, which will be a contributing factor for central bankers when considering the timing for easing monetary policy.

The December FOMC minutes were slightly hawkish, particularly compared to Powell's dovish press conference and the market's expectation of a March rate cut. The Committee emphasized a cautious approach, not ruling out future rate cuts if inflation progress is sustained, but also stressed the need to maintain a restrictive policy until inflation consistently moves towards their target. Discussions highlighted a balance between avoiding premature rate cuts and not maintaining overly tight conditions, with a focus on adapting to evolving financial conditions and inflation trends.

In December, Canada's services sector showed early signs of weakness, with a slight 0.1% rise in the PMI to 44.6, indicating continued contraction. The new business index fell to 45.3 amid high-interest rate pressures, and despite a steady employment index at 49.3, the overall data points to sustained sectoral weakness.

The US-led naval force in the Red Sea has intercepted 19 Houthi-launched drones and missiles in under a month, yet Houthi aggression persists. This ongoing conflict, despite US and allied warnings of potential retaliation, has disrupted global shipping, with many operators opting for longer, costlier routes. This has led to a significant increase in shipping rates, highlighting the broader economic impact of the continued instability in this key maritime passage.

ON DECK FOR NEXT WEEK:

On Tuesday, the NFIB survey will provide insights into the health of US small businesses for December. The major focus, however, will be on the US inflation data, specifically the Consumer Price Index (CPI), set to be released on Thursday morning. This is anticipated to show continued improvement (lower inflation) and will play a significant role in shaping near-term expectations for interest rates.

Inflation updates out of Europe and China are also scheduled as are updates on the Balance of Trade for most advanced economies.

For more information, please visit ci.com.

IMPORTANT DISCLAIMERS

This document is provided as a general source of information and should not be considered personal, legal, accounting, tax or investment advice, or construed as an endorsement or recommendation of any entity or security discussed. Every effort has been made to ensure that the material contained in this document is accurate at the time of publication. Market conditions may change which may impact the information contained in this document. All charts and illustrations in this document are for illustrative purposes only. They are not intended to predict or project investment results. Individuals should seek the advice of professionals, as appropriate, regarding any particular investment. Investors should consult their professional advisors prior to implementing any changes to their investment strategies. Certain statements contained in this communication are based in whole or in part on information provided by third parties and CI Global Asset Management has taken reasonable steps to ensure their accuracy. Market conditions may change which may impact the information contained in this document. CI Global Asset Management is a registered business name of CI Investments Inc. © CI Investments Inc. 2024. All rights reserved