The Fed Just Lost the Plot: Recession Risks Escalating

Duncan Presant - Jun 22, 2022

This past week has seen a material shift in markets and market outlooks. At the epicentre of the storm are the U.S. bond market and the Fed, which seems to have lost the plot.

This past week has seen a material shift in markets and market outlooks. At the epicentre of the storm are the U.S. bond market and the Fed, which seems to have lost the plot.

Where we were

Our base case until last week was the Fed pivot towards tightening policy that began last November had successfully guided the U.S. yield curve to price in rate risesto a level consistent with a move towards neutral by year-end. Neutral is thought to be around 2.5%, and U.S. bond yields were trading in the 2.5-3% range with the overnight rate expected to catch up to the already priced 2.5% range by year-end. In our opinion, this would have been sufficient tightening and allowed time for GDP growth to decline on a path consistent with a non-recession soft landing in 2023. It would also allow for inflation to trend back below 3% and towards the 2% target range in 2023/24. Central to our view is the U.S. (and Canadian) economy remains in good shape, but growth drivers (fiscal transfers and pent-up demand) are fading heading into 2023. What’s more, elevated debt levels leave the economy quite interest rate sensitive so even at the expected 2.5% neutral rate, monetary policy would be a headwind. That pace, while wildly faster than expectations only six months ago, still built-in time for inflation data to improve on the back of slowing growth and easing supply constraints. The process has already started but remains slow and was only expected to see more significant traction from recent policy shifts into the fourth quarter. Monetary policy works with a lag, there is no instant gratification! That was until this week…

What changed?

On Friday (June 10) U.S. CPI data came in a touch above expectations. Core CPI fell from 6.2% to 6% versus expectations of a drop to 5.9%. A very modest miss, but still headed in the right direction. Headline CPI rose to 8.6% from 8.3% versus expectations of it being flat. Not good, but not a huge surprise with the recent rise in gas prices a key culprit, and one that is beyond the control of the Fed (which is why it focuses on core measures in the first place). Although not great data, it’s nothing out of the range of normal variability. Then on Monday, the Wall Street Journal published an article indicating the Fed would raise rates by 75bps instead of the previously guided 50bps last week. Importantly, the article was written by a journalist known to ‘leak’ Fed news and it was, correctly, seen to have come straight from the Fed. Bond markets exploded, with U.S. rates pushing up to the 3.5% range. In our opinion, rates around 3.5% are way above any estimate of neutral and if sustained will tip the economy into a recession in the coming year. On Wednesday, the Fed did raise rates by 75bps and guided a more hawkish path for interest rates with an expected fed funds rate of 3.4% by year-end, and a 3.8% terminal rate in 2023, which is substantially higher and faster than previous guidance. This is a mistake, in our view, and will, if followed, put the economy into recession in 2023, bring down inflation and increase unemployment. Solving the recent inflation problem, driven mostly (but not completely) by aspects beyond central bank control, by “killing the patient” is not our definition of success. By accelerating the path of rate increases rapidly beyond neutral, the Fed has lost the ability to observe how the already enacted forces slowing the economy and inflation will play out before pushing beyond neutral. This tightening path is now like a pile on designed to aggressively slow an already slowing economy without the ability to adjust course in a timely manner. By the time evidence mounts the Fed has gone too far, it will be even further down the tightening path, well beyond the point of being able to pull back in time to avoid a recession. To borrow a phrase from Deng Xiaoping: The challenge the Fed is facing is akin to crossing a river by feeling the stones. If you try to run, you will fall in. Now what? While the recent market volatility will settle down in coming days, the path forward has become significantly more challenging, and our base case is no longer a soft landing. We now see a significantly higher risk of recession next year. Avoiding that outcome will require the Fed to back off from its current expected policy path and the rates market to reprice a more modest rate cycle. This can only occur once there is compelling evidence inflation is falling back towards the Fed’s 2% target. The rapid pace of expected rate hikes does not leave a lot of time for the inflation data to ease before the Fed will have gone too far. There is a high probability by the time the inflation data improves, the extra tightening in the pipeline will continue to push the economy over the edge given the lags associated with transmission of monetary policy into the real economy.

Market outlook

The path for equity markets will follow a different timeline. We expect a tough summer of volatile markets, much as we have seen so far this year. Up until now, markets had been pricing a return to neutral in rates. Now they must also discount the higher rate path laid out. One could argue the past week’s sell off already accomplished this, so some of the pain has been inflicted. But we expect over the summer, before we see an inflation drop and Fed repivot, analysts will start building higher recession probabilities into their earnings outlook. We expect as earnings estimates are revised downwards in coming months, there will be further downside pressure on markets. With equities already in bear market territory the downside from current levels is more modest. Keep in mind markets will bottom well before the economy does, and we expect as the inflation data improves and expectations for the Fed hiking path ease, equity markets will bottom and start to grind higher. We think this will likely unfold later this year, not in 2023. Our roadmap today is to buckle up for a further tough few volatile months over the summer, and to look for signs to add to exposures as we go into the fall. With markets already in bear market territory we are in the process of setting the base from which the next bull market will be built.

So, what to do?

Early this week, with the spike in rates towards 3.5%, we began to add to our bond weights in our multi asset strategies from long-held underweight levels, funded by trimming our equity weight. We simply do not see rates at 3.5% as sustainable in today’s economy and would expect both rates and risk markets to begin discounting increased recession probabilities over the summer. In the last hiking cycle into 2018, the Fed barely got rates above 2.25% and the 10-year topped at 3.25% before heading back below 1%. While the Fed forecast now is for rates to increase towards 4%, recall just a few months back it had only forecast a couple of rate hikes in 2022! The world seldom unfolds as the Fed expects and as the data evolves, so will both our and the Fed’s views. We await the next dovish Fed pivot. It won’t be a long wait and we will continue to manage our multi asset strategies tactically for the benefit of long-term investors.

A month ago, we wrote a piece with five key messages for investors concerning the recent volatility. Message number one was ‘a resounding Don’t Panic. For long term investors the secret to building wealth has always been about compounding returns in the markets over years and decades, a process that has always entailed riding through both ups and downs with ample evidence to show that those who try to time the bumps along the way tend to be worse off than those who stick with their long-term investment plans.’

That key message still applies.

At this time, we encourage investors to maintain diversification, incorporate flexible products that can take advantage of volatility and ensure their asset mix matches their time horizon and risk tolerance. Investing through volatility can be challenging but we know from the figures below overtime markets go up and timing the market is challenging.

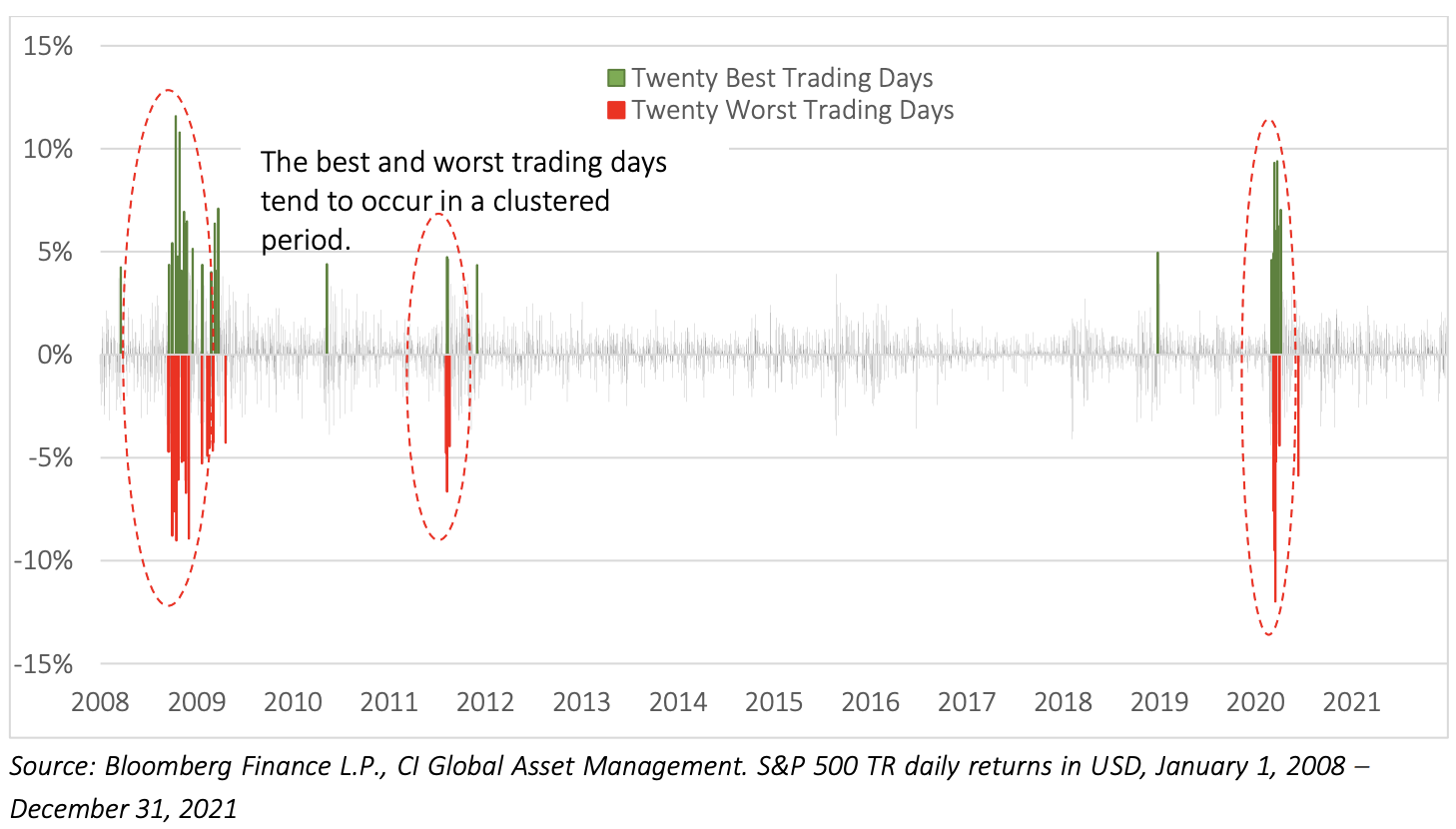

Figure 1: Resist the urge to time the market

This graph shows the best trading days in green and the worst in red from 2008 to 2021. Historically after a large drawdown there are typically large positive days around the corner. Negative volatility can be frightening; however, volatility tends to happen in clusters.

Figure 2: Don’t miss the best days

The below graph illustrates the challenge with trying to time the market. Despite the drawdowns that come with investing, had you stayed invested in the S&P500 Composite fully for 30 years you would be far better off, an investment of $100,000 would have grown to $2,081,229 at the end of 2021. If you tried to time the market and missed 10 of the best trading days your investment would have grown to only $953,518, missing out on $1,127,711 of growth! This is an important visual to reinforce that you don’t want to panic and sell at lows as the best positive days can compound return and make a large difference in the ending value of your portfolio.

For more information, please visit ci.com

IMPORTANT DISCLAIMERS:

Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments. Please read the prospectus before investing. Mutual funds are not guaranteed, their values change frequently, and past performance may not be repeated. This document is provided as a general source of information and should not be considered personal, legal, accounting, tax or investment advice, or construed as an endorsement or recommendation of any entity or security discussed. Every effort has been made to ensure that the material contained in this document is accurate at the time of publication. Market conditions may change which may impact the information contained in this document. All charts and illustrations in this document are for illustrative purposes only. They are not intended to predict or project investment results. Individuals should seek the advice of professionals, as appropriate, regarding any particular investment. Investors should consult their professional advisors prior to implementing any changes to their investment strategies. Certain statements contained in this communication are based in whole or in part on information provided by third parties and CI Global Asset Management Inc. has taken reasonable steps to ensure their accuracy. © 2022 Morningstar Research Inc. All Rights Reserved. The information contained herein: (1) is proprietary to Morningstar and/or its content providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete, or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information. Past performance is no guarantee of future results. The opinions expressed in the communication are solely those of the author(s) and are not to be used or construed as investment advice or as an endorsement or recommendation of any entity or security discussed. Certain statements in this document are forward-looking. Forward-looking statements (“FLS”) are statements that are predictive in nature, depend upon or refer to future events or conditions, or that include words such as “may,” “will,” “should,” “could,” “expect,” “anticipate,” “intend,” “plan,” “believe,” or “estimate,” or other similar expressions. Statements that look forward in time or include anything other than historical information are subject to risks and uncertainties, and actual results, actions or events could differ materially from those set forth in the FLS. FLS are not guarantees of future performance and are by their nature based on numerous assumptions. Although the FLS contained herein are based upon what CI Global Asset Management and the portfolio manager believe to be reasonable assumptions, neither CI Global Asset Management nor the portfolio manager can assure that actual results will be consistent with these FLS. The reader is cautioned to consider the FLS carefully and not to place undue reliance on FLS. Unless required by applicable law, it is not undertaken, and specifically disclaimed that there is any intention or obligation to update or revise FLS, whether as a result of new information, future events or otherwise. CI Global Asset Management is a registered business name of CI Investments Inc.

©CI Investments Inc. 2022. All rights reserved.

Published June 17, 2022.