Market Pulse - The week in review

Duncan Presant - Nov 09, 2022

THIS WEEK’S RECAP: ▪ The Federal Reserve delivered the expected 75 basis points (bps) increase to its funding rate, bringing it to 3.75%.

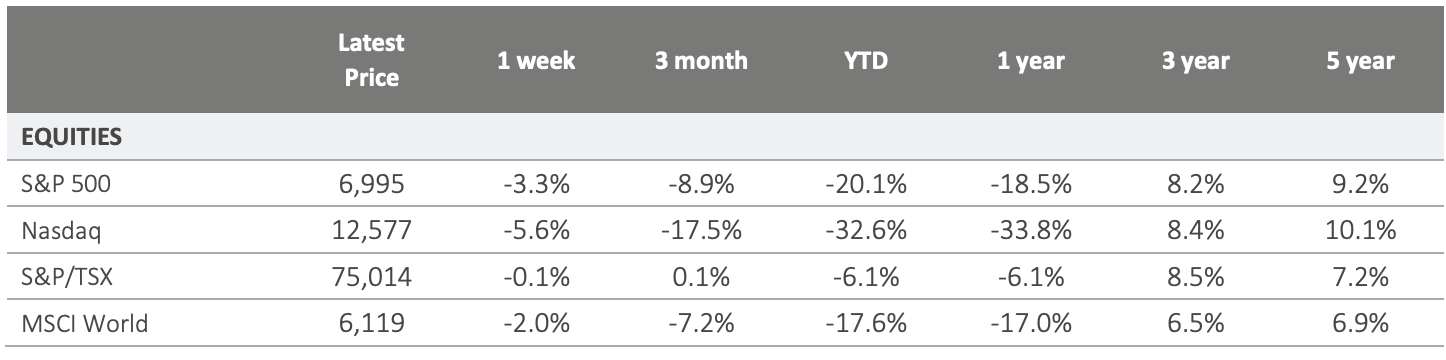

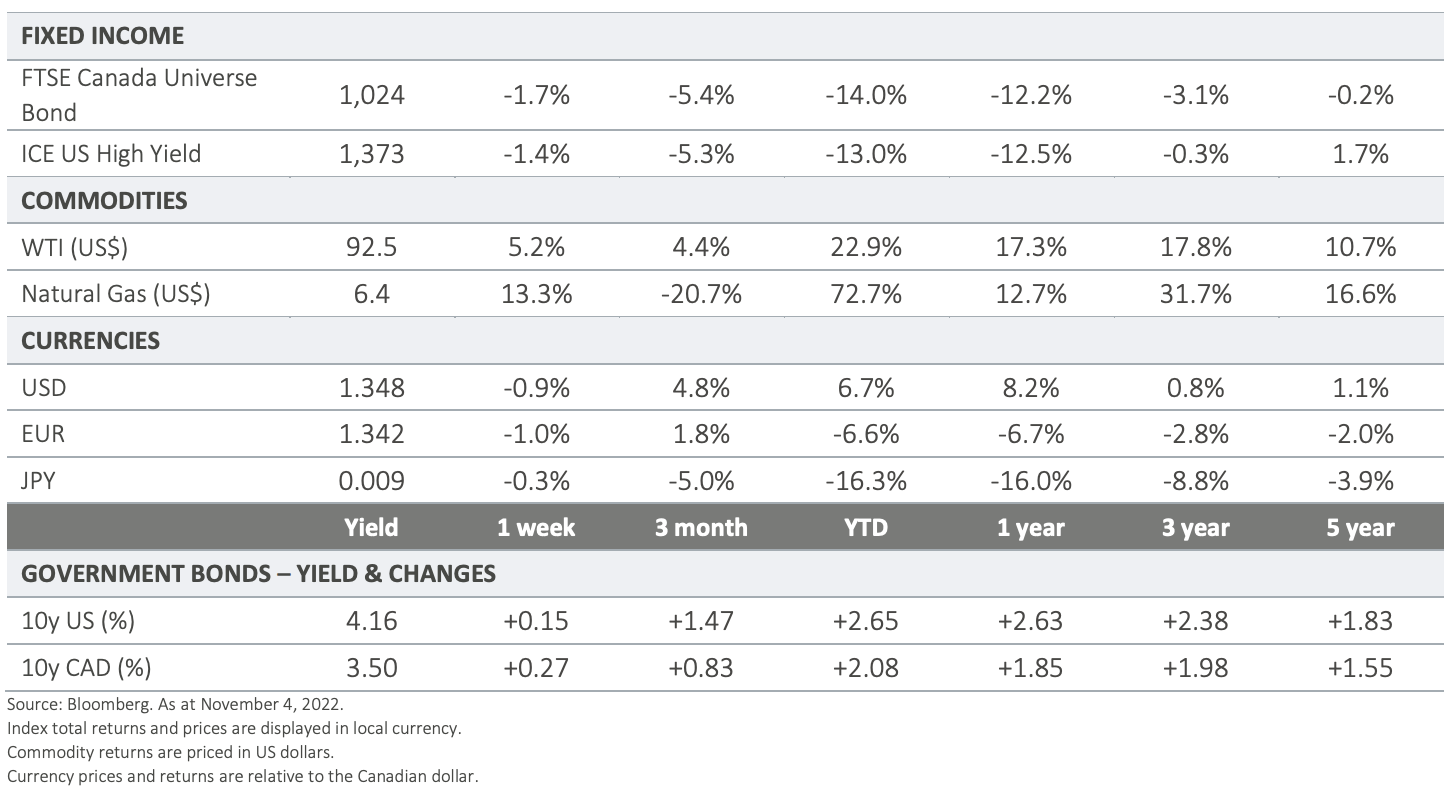

THIS WEEK’S RECAP: ▪ The Federal Reserve delivered the expected 75 basis points (bps) increase to its funding rate, bringing it to 3.75%. The important thing to note is the clash between the press release that stated that “the Committee will take into account the cumulative tightening of monetary policy, the lags with which monetary policy affects economic activity and inflation, and economic and financial developments” and Chairman’s Powell press conference where he was noticeably more hawkish and said that talks about a pause in rate hikes were premature. While the press release adopted a tone in-line with the one used by other central banks (Canada, Europe, UK and Australia), which would have been supportive for markets, the Chairman’s comments left the markets confused, causing a sell-off in equities and an increase in bond yields.

▪ As we have discussed over the last weeks, policy transmission lags are a crucial element of the ongoing dynamics. We know that official measures of employment and inflation will not respond immediately to the significant tightening in monetary policy, but despite a strong headline number, we believe that the US job numbers released on Friday shows some weakness beneath the surface, with the unemployment rate ticking up and a fall in full-time employment. This combines with several more reactive economic releases this week that are confirming that the economy is decelerating and that price pressures are waning. Given the confusion that followed Wednesday’s announcement, it is difficult at this stage to gauge how much deterioration the Fed will have to see before adjusting its rate path. Markets are likely to remain volatile until more visibility comes from either central bankers or from economic releases.

▪ In Canada, the employment numbers smashed expectations, with a creation of 108k jobs (120k full-time) and a downtick in the unemployment rate at 5.2%. On Thursday, the federal government delivered its fall economic update. The government acknowledged the economic slowdown and that the risk of a recession is noneligible. The most notable measure announced was a 2% tax on share buybacks, twice the tax rate that the US has recently announced. This measure won’t come in effect before 2024. The impact of that measure is likely going to be relatively muted for companies that purchase modest amounts of shares at reasonable multiples. The short-term impact is likely going to be an increase in buyback pace between now and the tax implementation date, although the pace of buybacks is likely to remain primarily driven by overall market and economic conditions.

ON DECK FOR NEXT WEEK: ▪ The next read of US inflation will be released Thursday morning, with a mild pullback expected. Though the Federal Reserve has indicated they are monitoring various measures of inflation, the market tends to have an outsized reaction to CPI data, and how it may impact the interest rate landscape going forward. This is the first of two CPI measures to be released between now and the next Federal Reserve meeting, scheduled for December 14, 2022.

▪ Tuesday is the US mid-term election day. Polls and models are currently hinting at a 75% chance that both the House and Senate will be controlled by Republicans. Election Day results have shown how they can depart from projections, but the most likely outcome is some form of political gridlock. That is typically not bad for markets, but in the current context it means that the policy response to any significant slowdown or recession would likely have to be monetary.

▪ Finally, we will be keeping an eye on China, where there are increasing signs that we might be seeing a loosening in the COVID-zero policy. If this does come to fruition, it would provide investors with a sense of comfort on supply-side dynamics for global inflation.

For more information, please visit ci.com.

IMPORTANT DISCLAIMERS This document is provided as a general source of information and should not be considered personal, legal, accounting, tax or investment advice, or construed as an endorsement or recommendation of any entity or security discussed. Every effort has been made to ensure that the material contained in this document is accurate at the time of publication. Market conditions may change which may impact the information contained in this document. All charts and illustrations in this document are for illustrative purposes only. They are not intended to predict or project investment results. Individuals should seek the advice of professionals, as appropriate, regarding any particular investment. Investors should consult their professional advisors prior to implementing any changes to their investment strategies. Certain statements contained in this communication are based in whole or in part on information provided by third parties and CI Global Asset Management has taken reasonable steps to ensure their accuracy. Market conditions may change which may impact the information contained in this document. CI Global Asset Management is a registered business name of CI Investments Inc. © CI Investments Inc. 2022. All rights reserved

For the full article please visit: https://ci-arena.ci.com/od/0ba3555f